The Oil & Gas Regulatory Authority (OGRA) of Pakistan has issued its ‘State of the Regulated Petroleum Industry’ report for the fiscal year 2019-20.

The report describes the challenges and performance for the oil sector, and the Natural Gas, liquefied petroleum gas (LPG), liquefied natural gas (LNG), and compressed natural gas (CNG) sectors.

Oil Sector

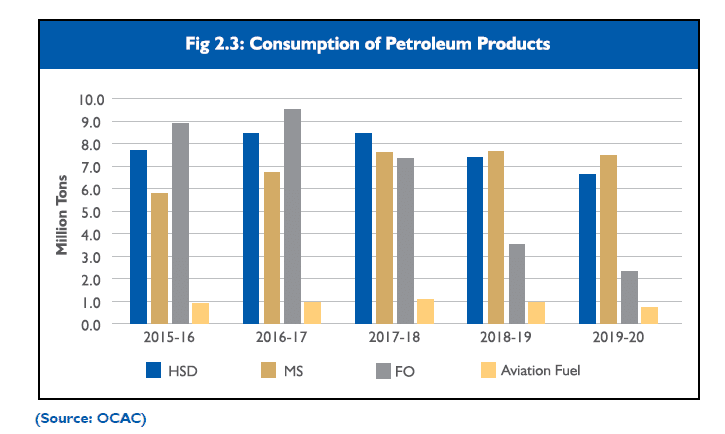

Pakistan’s oil sector has faced major challenges due to the unprecedented crises caused by the COVID-19 pandemic. During the fiscal year 2019-20 (FY20), the import of crude oil and petroleum products had declined by 26.42 percent and 7.60 percent to 6.77 million tons and 8.10 million tons respectively as compared to the previous year’s imports of 9.21 million tons and 8.77 million tons.

Accordingly, the refineries’ productions had declined by 20.43 percent to 9.86 million tons as compared to 12.38 million tons, and consumption by 11.98 percent to 17.63 million tons as compared to 20.03 million tons in FY 2018-19.

PARCO had held its position at the top among all the local refineries in the production of petroleum products during FY 2019-20 with a 29 percent share (2.85 million tons) of total production, followed by BPPL with 22 percent (2.13 million tons), ARL & NRL with 16 percent (1.56 million tons) each, and PRL with 12 percent (1.21 million tons).

The product-wise production shows that HSD had the highest share of 40 percent (3.79 million tons) in the total refineries production, followed by FO with over 23 percent (2.22 million tons), and MS with around 21 percent (1.98 million tons) during FY 2019-20. These three POL products had accounted for around 85 percent (7.99 million tons) share in total refineries’ production.

ALSO READ

Rupee Finally Posts Blanket Gains Against All Major Currencies

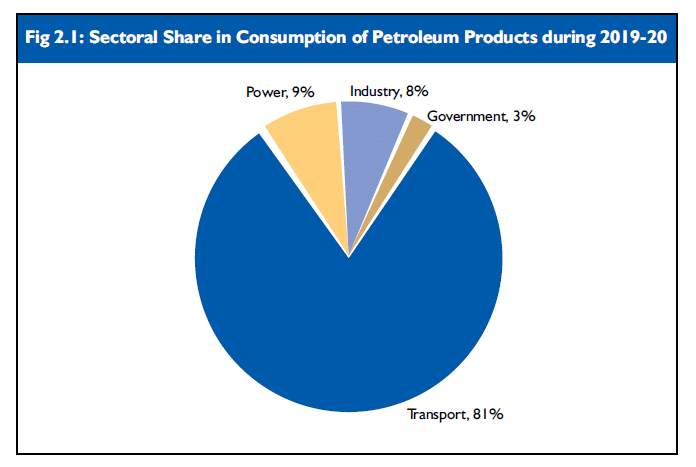

The consumption of petroleum products in the power sector had suffered a huge decline of 43.5 percent to 1.52 million tons during FY 2019-20 as compared to 2.76 million tons during FY 2018-19 due to the shifting of power generation from FO to RLNG, followed by the government where consumption had declined by 10 percent, transport by 5.6 percent, and industry by 5.5 percent.

In the marketing arena, energy products had a change in the market share as compared to the previous year. PSO had been the major shareholder with the highest market share and had gained around three percent (from 41 percent to 44 percent) during FY 2019-20.

Hascol had lost around four percent market share from 10 to 6 percent.

Natural Gas

Natural gas is a major contributing fuel to Pakistan’s energy mix. The demand for natural gas, particularly by the residential, fertilizer, and power sectors has also increased over the years, putting more pressure on the limited indigenous gas supplies.

The indigenous gas production had declined by 10 percent. During the year in concern, it had come down to 2,138 MMCFD from 2,379 MMCFD in the previous year. On the other hand, gas consumption had declined by six percent, coming down to 3,714 MMCFD from 3,969 MMCFD.

The deficit between production and consumption had been met partially through RLNG imports whose share in natural gas supplies has increased from 27 percent to 29 percent during the current financial year.

Pakistan has a huge transmission network of 13,452 km and a distribution network of 177,029 km gas pipelines that provide natural gas to the domestic, industrial, commercial, and transport sectors.

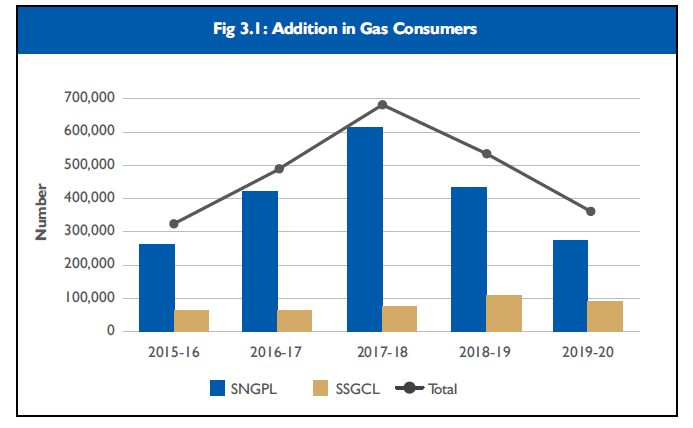

The gas utility companies have expanded their transmission and distribution networks to cater to the demands of their new consumers. The SNGPL and the SSGCL had extended their transmission networks by 190 km and 72 km respectively during FY 2019-20. Similarly, the SNGPL had extended its distribution network by 5,731 km, and the SSGCL by 527 km during the same period.

The SNGPL had connected 271,228 new consumers during FY 2019-20, reaching a total of 7.0 million consumers in its network. Additionally, the SSGCL has added 95,011 new connections, making a total of 3.1 million consumers in its network. Overall, there had been 10.12 million natural gas consumers in the country by the end of the financial year 2019-20.

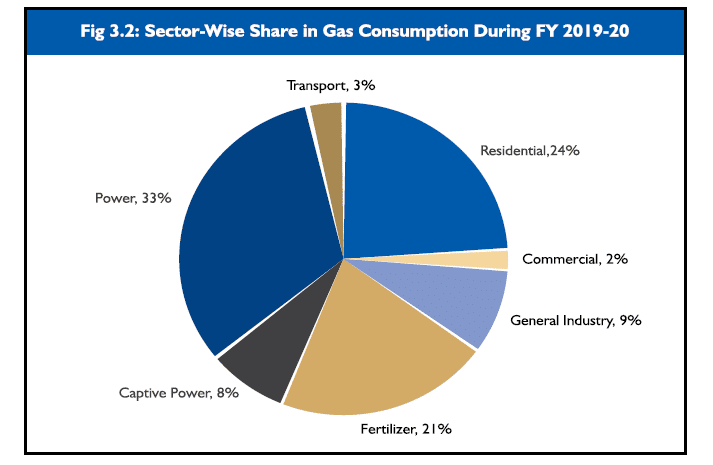

The main consumer of natural gas had been the power sector, consuming 33 percent (1,198 MMCFD), followed by the domestic sector with 24 percent (888 MMCFD), fertilizer — 21 percent (779 MMCFD), General Industry — nine percent (327 MMCFD), and captive power — eight percent (290 MMCFD) of the total gas consumed during FY 2019-20.

The province-wise gas consumption shows that the Punjab’s share had been 56 percent (1,471 MMCFD), Sindh — 33 percent (874 MMCFD), Khyber Pakhtunkhwa (KP) — nine percent (249 MMCFD), and Balochistan — two percent (48 MMCFD) of the total gas consumption during the year under review.

The supply of natural gas supply during the year had been 4,052 MMCFD and was mainly contributed by the major gas fields Mari, Sui, Uch, Qadirpur, Kandhkot, and Maramzai. Of the total supplies, 1,057 MMCFD of gas had been supplied by the gas fields/producers directly to their consumers and the remaining through gas utility companies.

Sindh’s share in gas supply had been 45 percent (1,344 MMCFD), whereas KP, Balochistan, and Punjab had supplied 12 percent (368 MMCFD), 11 percent (335 percent), and three percent (91 MMCFD) respectively. The remaining 29 percent (857 MMCFD) of gas supplied was imported LNG.

The demand-supply gap during FY 2019-20 had been 1,349 MMCFD, which is expected to rise to 4,229 MMCFD by FY 2030-31.

ALSO READ

Pakistan’s Foreign Exchange Reserves Break All Historic Records

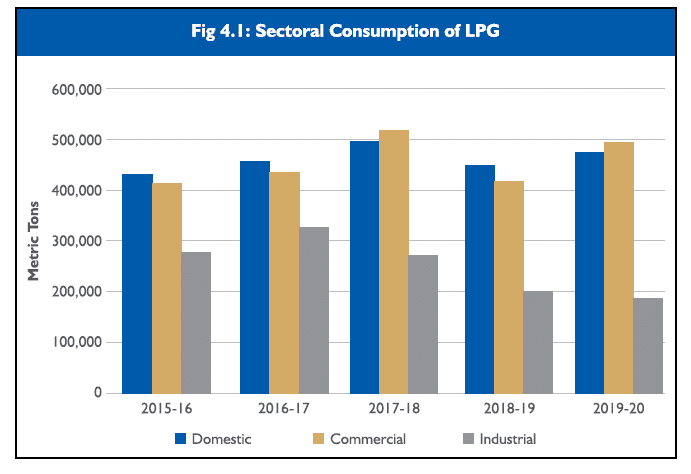

LPG Sector

The LPG share in Pakistan’s primary energy supplies is around one percent. The current size of the LPG market is around 1,149,352 MT/Annum, which is 8.28 percent higher than last year’s 1,061,448 MT/Annum.

A major increase in the LPG consumption of around 19 percent (from 415,368 to 492,968 M. Tons) had been observed in the commercial sector, followed by the domestic sector, which had increased by six percent (from 445,497 to 472,056 M. Tons) during FY 2019-20 as compared to FY 2018-19.

LPG consumption in the industrial sector had declined by eight percent (from 200,583 to 184,328 M. Tons) during the same period. Refineries, gas-producing fields, and imports are three main sources of LPG supply in the country.

The production of refineries and gas fields had accounted for 68 percent of the LPG consumption, whereas the remaining 32 percent had been imported during FY 2019-20. LPG supplies had increased by four percent during FY 2019-20, mainly on account of a 39 percent increase (from 252,467 to 350, 096 M. Tons) in LPG imports as compared to last year.

Conversely, the supplies from refineries and fields had declined by 20 percent (from 201,322 to 161,434 M. Tons) and two percent (from 607,108 to 593,061 M. Tons) respectively during the same period.

There had been 11 LPG producers and 208 LPG marketing companies with more than 7,400 authorized distributors by the end of FY 2019-20. Furthermore, there had been 22 operational LPG auto refueling stations within the country.

The OGRA has also pre-qualified 56 LPG equipment manufacturing companies as authorized manufacturers of LPG equipment.

LNG Sector

Liquefied Natural Gas (LNG) is natural gas that is cooled and converted into liquid at a temperature of -162°C (−260°F) and atmospheric pressure. Liquefaction reduces fuel volume by about 600 times and allows it to be stored and transported in specially designed vessels.

In an effort to bridge the widening natural gas demand-supply gap in the country, the first LNG re-gasification terminal had been commissioned in March 2016 and the second LNG terminal was commissioned in April 2018.

The government has mandated the state-owned companies Pakistan State Oil (PSO) and Pakistan LNG Limited (PLL) to import LNG on its behalf. PSO has signed a Government-to-Government contract with Qatar Gas for a period of 15 years, whereas PLL has shorter-term LNG contracts with Gunvor and Shell.

LNG imports during FY 2019-20 had declined by five percent quantum-wise to 857 MMCFD from 901 MMCFD in FY 2018-19, but its share in the overall natural gas supplies had increased from 27 percent last year to 29 percent as of now.

ALSO READ

SECP Imposes Rs. 500,000 Penalties on Pakistan Engineering Company Ltd and its CEO

CNG Sector

The OGRA has played a vital role in the promotion of CNG in the transport sector and the setting of higher standards for the safe operation of CNG stations.

The use of CNG as an alternate fuel in the transport sector has helped to reduce air pollution to a considerable extent, which also includes excessive suspended particulate matter (SPM) emitted from public transport vehicles and private vehicles.

Natural gas consumption in the transport sector has gradually declined over the years due to dwindling indigenous gas production. During FY 2019-20, the natural gas consumption in the transport sector had declined from 178 MMCFD in FY 2018-19 to 127 MMCFD.

The OGRA has always prioritized safety and quality with regard to the certification of local and foreign CNG equipment.

Furthermore, in order to promote the indigenous production of CNG equipment, the OGRA has granted permission for the manufacturing/assembling of CNG Compressor, Dispenser, and Conversion kits for vehicles subject to the conformity of the laid down international technical standards.

Stay Connected with ProPakistani

Get the latest automobile news, car launches, bike reviews, videos and analysis wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.