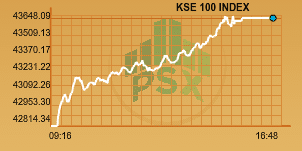

PSX’s benchmark index KSE – 100 has surged more than 840 points during the day, after losing more than 297 points yesterday succumbing to selling pressure from short term investors taking advantage of the recent rally in stocks.

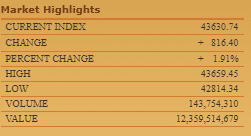

At the end, the benchmark index saw a gain of 816 points or +1.91% to close at 43,630.40 points.

Commercial Banks lead the points table with Bank of Punjab BOP +4.55%, MCB Bank Ltd. MCB +2.23%, and Habib Bank Ltd. HBL +2.26 topping the list.

Major contributors of the market were HBL +69.89, ENGRO +52.17 points, UBL +42.10 point and MCB with +42.10 points.

Oil and gas sector with exploratory companies were all up over the increase in International Oil prices which help up to bring the gain in the market.

Auto Sector saw huge gain as most of the companies increased their prices of the vehicles.

Whereas Fertilizers and the Chemical were also the big gainers as well as ENGRO was up by +3.04%, FFBL +2.93% and FFC +1.92% . In chemicals ICI was up by +3.69% and WAHN was up by +5% at the bourse today.

Chemicals have been going up as Petrochemicals prices have been raising on the back of increase in crude prices as Ethylene in South East Asia was reported at USD1290/ton in the first week of Jan-18. This shows an upsurge of 6% compared to average price of Dec-17. On the other side PVC prices clocked in at USD 885/ton reporting an increase of 2% as compared to average of Dec-17.

Cement Stocks continue to remain buoyant as ACPL +2.13%, CHCC +2.39%, FCCL +2.52%, MLCF +4.57% and PIOC +2.45% contributing most points to the index tally.

As per the data released by APCMA, total cement dispatches for the month of Dec’17 arrived at 3.73mn tons versus 3.55mn tons recorded in the same month of last year – a growth of 5%YoY.

During the month, local dispatches clocked in at 3.40mn tons, depicting a decent growth of 7%YoY, whereas exports plunged to 0.33mn tons as against 0.37mn tons recorded in the same month of last year, down 11%YoY.

Foreign Buying was seen during whole week as well as well International buyers are coming back in the market. Finally, the foreign interest in local equities could also be a determining factor in setting the direction of the market.

TRG reported FY17 LPS of Rs8.0, which is over 4x lower than LPS reported in FY16 of Rs1.5. On quarterly basis, TRG reported LPS of Rs5.6 for 4QFY17 compared to EPS of Rs0.3 last year.

The steep decline in earnings primarily stems from higher administrative and general expenses, which were Rs11.2bn for FY17, up 1.3x over last year’s Rs4.9bn. Further, the company booked Rs5.6bn under this head in 4Q alone. We await management clarity on this expense, which looks like a one-time amount. Normalizing this amount would have resulted in LPS of Rs4.0 for FY17.

Volumes are getting better day by day as all shares index had a traded volume of 327.76 million shares today. Overall, stocks of 385 companies were traded on the exchange, of which 298 gained in value, 68 declined and 19 remained unchanged. In KSE 100, 143.75 million shares were traded with a net worth of just Rs. 12.35 billion.

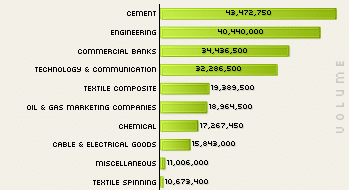

Top traded sectors:

Aisha Steel Mill was the volume leader with 16.91 million shares, up by Rs. 1.00 to close at Rs. 20.77. It was followed by TRG Pak Ltd with 16.72 million shares, gaining Rs. 1.53 to close at Rs. 32.31, Dewan Cement with 15.58 million shares, gaining Rs. 1.10 to close at Rs. 23.10 and Azgard Nine with 14.91 million losing Rs. 0.07 to close at Rs. 15.34.

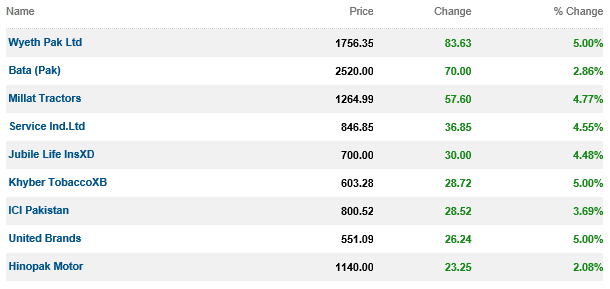

Top Advancers of the market were:

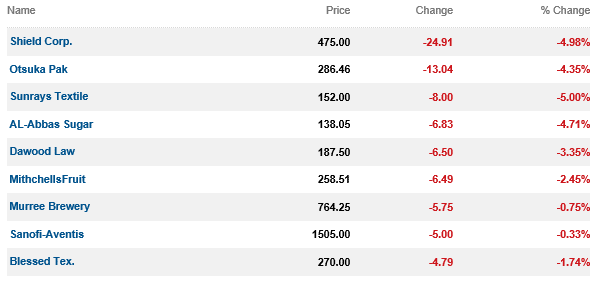

Top Decliners of the market were:

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.