Pakistan’s economy could grow by 1.8% in FY2020/21 driven by some recovery in private consumption. This was stated in a report which was released by the Institute of International Finance (IIF) by the name “Pakistan: Commitment to Reform Faces a Test.”

The report stated that the pandemic led to a contraction in output of 0.7% in FY2019/20 (ending June 2020). Domestic demand declined by 2%, while exports of goods and services have increased by 1.6% as compared with a decline of 7.3% in imports of goods and services.

Pakistan’s economy could grow by 1.8% in FY2020/21 driven by some recovery in private consumption.

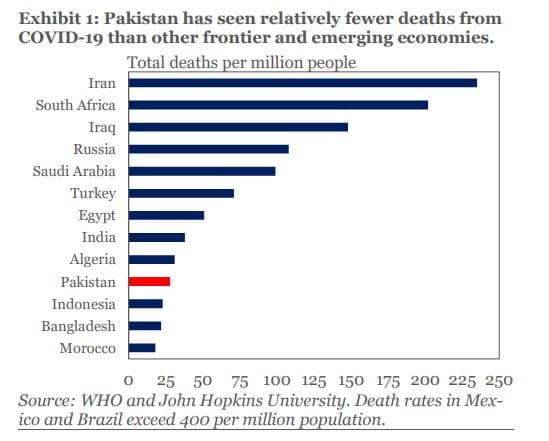

However, risks to the economic outlook are tilted to the downside, amid uncertainty regarding the magnitude and duration of the pandemic. Adjusted for population, fewer cases and deaths of COVID-19 have been recorded in Pakistan than in other developing and emerging economies.

These results are subject to a large degree of uncertainty, as data quality, testing capacity, and transparency vary, said IIF in its report. While the rate of new cases has recently declined, the pandemic still puts considerable stress on Pakistan’s public health system. As of mid-August, lockdown restrictions had been lifted across the country.

The response measures have been adequate, supported by the IMF’s emergency financing in the amount of $1.4 billion, provided in April 2020. The expansion of social programs has rightly focused on tackling the health emergency and supporting the most vulnerable while stimulating economic activity, added the report.

The State Bank of Pakistan’s (SBP) proactive liquidity initiatives and lower policy rates are propping up economic activity and safeguarding financial stability. The policy rate has been lowered 5 times since February, a cumulative reduction of 625 bps.

The authorities have also introduced a fiscal stimulus package in the amount of $5.1 billion (1.9% of GDP), which included direct transfers to wage workers and poor families, financial support to SMEs and the agricultural sector, higher subsidies for basic goods, and various tax incentives. One-third of this amount has been implemented already, and the remaining $3.4 billion will be used in the current FY 2020/21 budget.

Exchange rate flexibility is helping

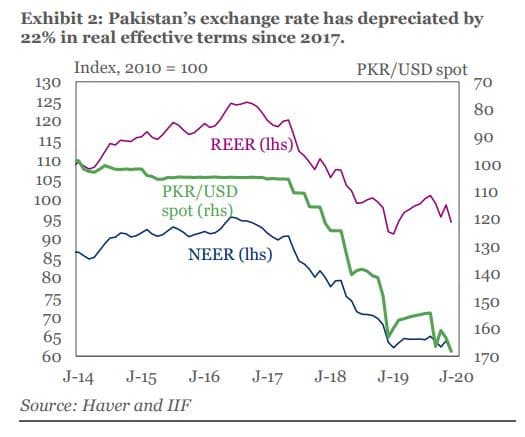

The sharp depreciation of the rupee has reduced external vulnerability, said IIF. Pakistan’s exchange rate is market-determined and has depreciated by 22% in real effective terms since 2017.

Institute of International Finance expects the policy rate to remain the same in the next MPC meeting, thus dampening inflationary expectations. The 12-month headline inflation was 9.3% in July 2020, y-o-y.

Although rising food prices continue to exert upward pressure on inflation, weak demand is likely to keep inflation in upper single-digit levels, said the report.

The external position is strengthening. The effects of currency depreciation and weaker domestic demand are visible, as imports dropped by 18% in nominal dollar terms, more than offsetting the decline in exports of 7%, in FY 2020 (July 2019 to June 2020).

Workers’ remittances, which slightly exceeded exports of goods, continued their increase, supported by a more depreciated exchange rate and appropriate policy steps implemented by the authorities, including reducing the threshold for eligible transactions from $200 to $100 under the Reimbursement of Telegraphic Transfer (TT)

Charges Scheme, increased use of digital channels, and targeted marketing campaigns to promote usage of formal channels.

The decline in the trade deficit combined with higher remittances narrowed the current account deficit from 4.8% of GDP in FY 2019 to 1.1% in FY 2020.

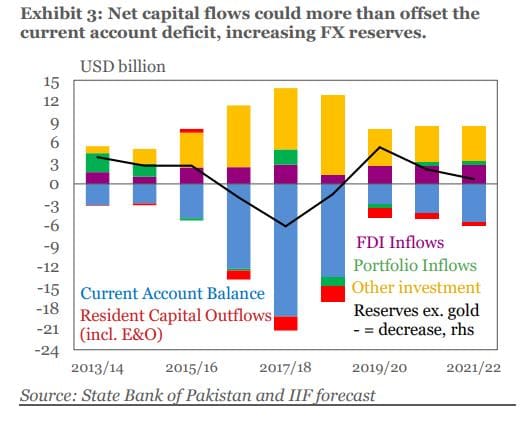

Net capital flows have more than offset the current account deficit, leading to a substantial increase in official reserves (excluding gold) to the equivalent of 2.8 months of import coverage, it added.

While the current account deficit may widen slightly to 1.6% of GDP due to some recovery in imports and slightly lower remittances in FY2021, the increase in net capital inflows will lead to a further rise in official reserves, said IIF.

Fiscal deficit to widen in FY 2021

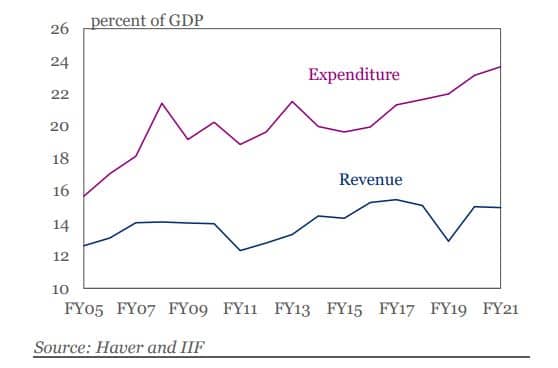

Large fiscal deficit, on the back of low tax revenue mobilization, and high public indebtedness remain major challenges, it noted.

Resistance to tax reforms and cost-recovery in the energy sector from entrenched elites could undermine the fiscal consolidation strategy and put public debt sustainability at risk, said the IIF. The completion of the second Extended Fund Facility (EFF) review has been delayed pending implementation of key reforms. The narrowing of the deficit in FY 2020(ending June 2020) to 8.1% of GDP was largely due to one-off factors, including the jump in profit transfers from SBP to the budget, which bolstered non-tax revenue. Spending increased by 15.6% due to sharp increases in interest payments on debt and social transfers.

The budget for the FY 2021 envisages cuts in subsidies, freezing salaries and pensions, and increases in petroleum levies. However, rising defense spending, higher interest payments (6.3% of GDP), and rollover of fiscal stimulus from FY 2020 could widen the deficit to 8.7% of GDP, compared with a budgeted deficit of 7%, which is based on growth of 2.1%. IIF said that the public debt could rise to 86% of GDP by June 2021, compared with 70% in 2018.

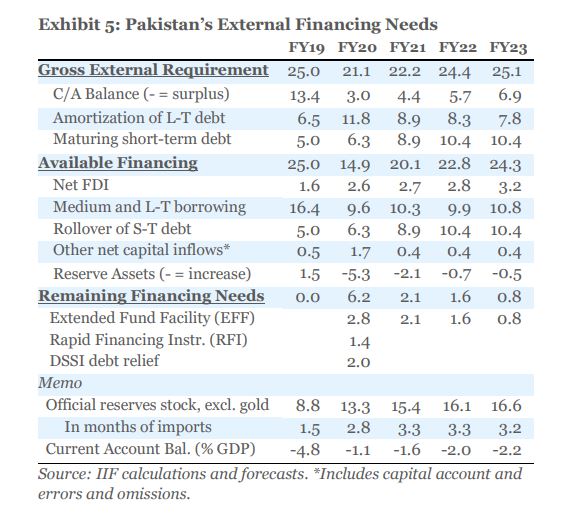

The external funding picture warrants caution as debt amortization remains high in years to come.

However, improvement in the current account, rollover of short-term debt, and Debt Service Suspension Initiative (DSSI) have eased Pakistan’s external financing needs and shored up its official reserves, which could increase further to $15.4 billion (excluding gold) by June 2021 (3.3 months of imports of goods and services), said the report.

The DSSI provided debt-service suspension to help Pakistan and other low-income countries to concentrate adequate resources on fighting the COVID-19 pandemic.

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.

No tower can stop Imran Khan. No cat can lure Imran Khan. A leader worthy to lead the world.

This will only happen if current Govt. is throw away right today.