Old timers would know the history and evolution of the broadband industry in the country, of how hundreds of smaller ISPs, telcos, startups and other stakeholders worked real hard and created a demand for high-speed broadband DSL in Pakistan.

It took these small companies over 10 years reach to a point where the groundwork was laid and a clear demand for DSL services surfaced, culminating in the start of a digital Pakistan. It was during this time that giant players — who were previously silently observing the whole game play as a part of their strategy — jumped into the ring with strong financial muscle that no one could compete with.

Resultantly, due to deep pockets of the giant players, innovation in service and particularly strategic market positioning, smaller ISPs and startups — who had initially built the ground for broadband — were wiped out of the business.

Being a witness of that bigger game, I foresee the same situation in Branchless Banking (BB) industry at present that currently thrives on the following two major revenue streams:

- Over the Counter (OTC): 80%

- Wallets: 20%

It is important to understand the dynamics of Branchless Banking offerings to comprehend the overall scenario. So let’s get back to the basics to figure out that why branchless banking was invented in the first place.

How Branchless Banking was Invented?

Across the globe, the financial services accessibility remained restricted to a small set of the overall population due to various regulatory and other due diligence requirements. This created a need for developing a separate program / infrastructure with relaxed criteria focusing on the financial requirements of relatively lower segments of the society and thus paved way for branchless banking (BB) set-up to serve the financial inclusion cause for masses in a much better and improved way.

According to the World Bank, around 2 billion people don’t use formal financial services and more than 50% of adults in under-privileged segment are deprived of banking services. Financial inclusion is pivotal for poverty alleviation. Research has shown that the population’s access to financial services also increases their chance for savings and can have large long-term benefits. The idea of “commitment savings”, which restricts individuals from withdrawing funds unless they have reached a particular level, results in increasing productive investment and consumption, raises productivity and incomes, and increases expenditures on preventive health. It can also hugely benefit in empowering women.

In light of the importance given to financial inclusion and its proven benefits in poverty reduction, Pakistan has also taken several steps in this regard.

Introduction of a regulatory framework for microfinance banks, establishment of a specialized microfinance Credit Information Bureau, launch of nationwide financial literacy programme and subsidized lending schemes are some of the initiatives taken under leadership of the State Bank of Pakistan that demonstrate the serious interest in this segment.

However, in comparison to other players in this region, Pakistan is still in the early stages of the life cycle and there is a huge room for improvement.

Financial inclusion is a key socioeconomic challenge and one that is of interest to international financial institutions, central banks, governments and policymakers alike. This is evident from the fact that the World Bank has set a goal to achieve universal financial inclusion by 2020.

Financial inclusion is not just about ensuring that consumers have formal financial accounts. It’s about ensuring that consumers can access tools which can change the course of their lives.

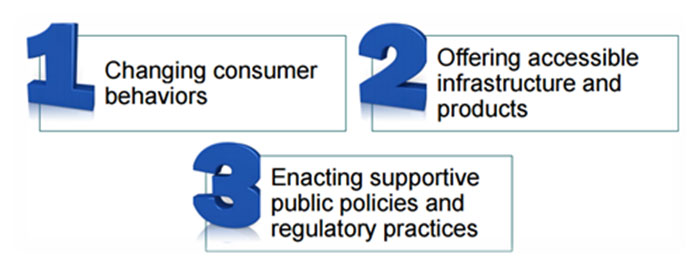

There are three main aspects to building financial inclusion:

Changing consumer behavior through building awareness.

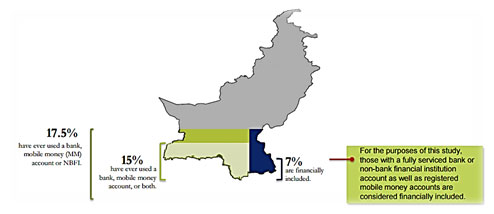

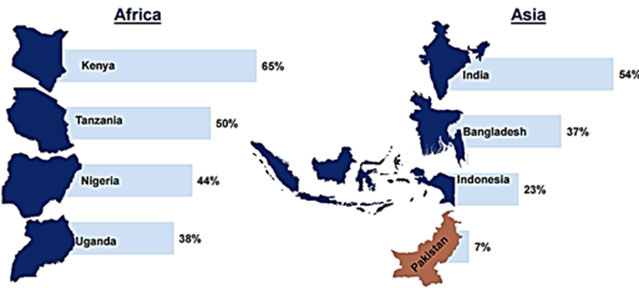

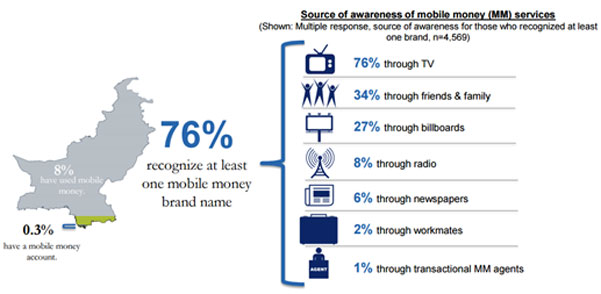

Pakistan had an abysmal percentage ranging between 7%-8% of customers having a conventional bank account at a financial institution in 2014 while this average stood at 45.5% for South Asia. This is clearly indicative of the state of financial inclusion in the country.

Other variables employed to measure the usage of financial services give a similar picture. Average borrowing from a financial institution was almost negligible at 1.5% whereas other South Asian markets stood at 6.4% for 2014.

Similarly, savings at a financial institution stood at a mere 3.3% for 2014 relative to the South Asian average of 12.7%.

Lack of awareness and trainings of such services is the biggest reason for such low percentages. The conventional belief of the larger population of the society on a tangible currency note as compared virtual space / cloud keeps them away from utilizing such services and maintaining their savings in their accessible reach.

Even the segment well-versed with virtual space did not utilize the potential of these services to their best.

The Future of Branchless Banking

So evaluating the entire scenario, one can easily understand that Branchless Banking market is currently going through the development phase and has a clear correlation with the Broadband industry.

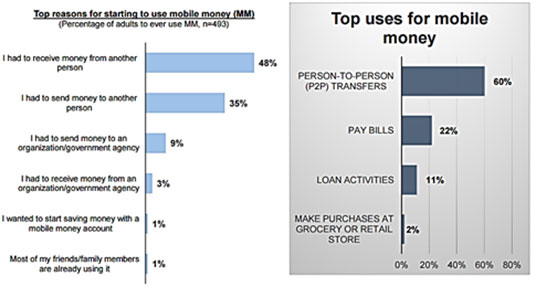

SBP recently announced its Financial Inclusion vision 2020, according to which they are planning to get 50 Million mobile wallets opened in next 4-5 years. Let’s evaluate this under the perspective where more than 8 Million wallets (including BISP wallets) have already been opened but only ~250K are active transacting customers. It’s unfortunate to see such a low number of users utilizing it.

Future projections based on this ratio would lead to the fact that transacting customers would remain at ~1 Million even if the total wallets reach 50 Million mark. While investments in the form of NFC Models, close loop payment ecosystem etc. have been made in this segment by start-ups and few major Telcos, the results are not too encouraging in terms of transacting customers.

This could be primarily because of the fact that people still believe in paying in cash, keeping tangible currency, using conventional banking tools (where possible). The lack of stronger checks in e-commerce industry further alleviates the problem since the community as a whole prefers to avoid online payments models against purchases.

Some 4-5 years from now, I foresee 2020 as the year by which behavioral changes and transformations in payment / spending mediums would take acceptable roots in the general society.

SBP is going to issue more and more licenses in PSP, BB space, with lots of new start-ups and corporate entities vying for the slice of the branchless banking space. There will be a time when masses will get their basic needs and requirements fulfilled through BB/PSP/Micro Finance players.

Imagine future scenarios where, through branchless banking:

- A small player would be offering Bicycles, Sewing Machines, Mobile Phones, & Motorbikes on lease

- Another small set-up offering credit cards, personal loans, business loans of smaller amounts

- Someone in the industry offering good saving rates on smaller investments.

Just imagine the size of documented economy at 50 Million wallets with only PKR. 5,000 average saving deposits. That’s the point when the big boys would like to make their entrance on the dancing floor and huge activities will be shown in BB/Micro Finance/PSP areas. So till then, let’s wait and see how soon and how successfully this market gets evolved and developed.

Data Sources: Market Feedback, Financial Inclusion Insights, SBP Data, Google and World Bank.

Writer is Branchless Banking Head in one of the Largest of banks of Pakistan. He has over 15 years of experience in Telecom, FMCG and Digital/Retail Banking industries.

Stay Connected with ProPakistani

Get the latest news, tech updates, telecom insights, and business stories wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.

Bhaar mein gaya article.

I strongly condemn the map provided at infographic chart! There is no Kashmir and even Gilgit-Baltistan.

Baqi article k baray main Kiya khayal hay?

ain’t nobody got time for that

why don’t you guys bother to read or review your own published articles before copy-pasting it?

Admin please post complete map instead of the one that you use in your article.

I agree, Amir Bhai please use the complete map.

I agree, Author please use the correct map

Had a gist. Nice Article

Good article

Good insights of BB covered in this article. In coming 5 years, we are expecting, establishment of ECO system for Wallets acceptance. This will be a game changer.

Can Admin/Poster of this article mention the reason behind not showing full map of Pakistan ?

Good article. I appreciate Branchless Banking being highlighted at any forum and as the Business Manager who launched OTC payments in the country, I’m happy to see the business moving from OTC to Mobile Accounts. The activity numbers quoted, however, are a bit off – please check the latest SBP reports. There should be at least 2 million unique active MA customers today.

One important area to investigate is, why aren’t people moving to Mobile Accounts? That is a question you all must ask yourself and answer honestly. Does the convenience and security of financial transactions from your own mobile phone not hold any attraction? Or do we not have the use cases in there for customers to use a Mobile Account? Or is it awareness?

The work that the entire industry and the SBP have done in creating Branchless Banking in Pakistan is nothing but amazing. Everybody in the world knows about what we’re doing in Pakistan – something to be extremely proud of. We should all be very happy to see the empowerment to the people of Pakistan and the number of jobs created in the market!

The primary reason for slow adoption of Mobile Accounts would be awareness/literacy level. When comparing with Kenya, our population is not comfortable with using USSD as a method of payment. In Kenya, people pay for everyday goods using nothing but dialing USSD menus. And M-Pesa is available every where. Which only shows that Kenyans are more tech savvy than us. Which leads me to conclusion that a lot of work is required to make Pakistanis comfortable in using Mobile Wallets before Mobile Wallets can take off. Some sort of awareness campaign is required at national level.

came to the comment section to see what other thought about branchless banking and got people complaining about a map. 11/10 will visit again.

Branchless banking? At least, make your debit cards work online.

cash free economy.

every mobile user must allow to do mobile paisa transactions equal to his salary without any sort of charges or tax.