The country’s e-banking transactions volume grew by 10.7 percent to 400 million during the second quarter of the fiscal year 2021-22, according to the State Bank of Pakistan (SBP).

As per SBP’s latest figures, the value of transactions through digital banking grew by 22.8 percent to Rs. 33 trillion. During the calendar year 2021, the volume of transactions increased by 41 percent to 1.4 billion, while the value of transactions increased by 45 percent to Rs. 106 trillion.

1/2 #SBP issues Q2FY22 report on Payment Systems that shows encouraging growth in digital banking. Overall e-banking transactions volume grew by 10.7% to 400mn whereas value by 22.8% to over Rs33tn. During CY2021 volume increased by 41% to 1.4bn and value by 45% to Rs106tn. pic.twitter.com/g9ONr76Lqt

— SBP (@StateBank_Pak) April 15, 2022

The State Bank of Pakistan released its second quarterly report of payment systems for the fiscal year 2021-22 today covering the period October – December 2021. The report presents an encouraging picture of the adoption of digital banking in the country.

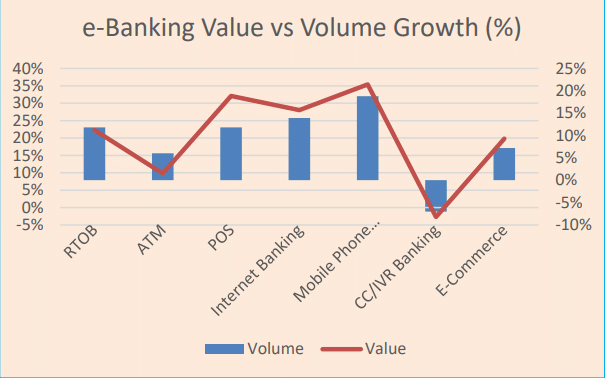

During the quarter under review, customers’ inclination toward the use of e-banking continued as it rose to 10.7 percent in volume and 22.8 percent in value of transactions on a Quarter-on-Quarter (QoQ) basis. E-banking includes transactions conducted via electronic channels including real-time online Branches, ATMs, mobile banking, internet banking, call center banking, POS and eCommerce. It would be pertinent to note that the growth in e-banking transactions is much steeper relative to paper-based transactions, albeit the value of transactions is higher in the case of the latter.

The volume and value of paper-based transactions increased by 3.4 percent and 12.2 percent respectively. While the volume of e-banking transactions is almost four times higher at 400 million than paper-based transactions at 101.4 million, the value of transactions of the former stands at Rs. 33.4 trillion compared with Rs. 41.6 trillion paper-based transactions.

All around, growth in e-banking included expansion in both mobile and internet banking with a double-digit increase in value and volume of transactions during the second quarter. The number of mobile banking transactions amounted to 94 million, while the value reached Rs. 2.2 trillion, which comes to 18.8 percent and 35.4 percent growth respectively on a QoQ basis.

Meanwhile, the number of mobile banking users grew by 5 percent on a QoQ basis, reaching a total of 11.9 million users. The internet banking users reached 6.9 million, conducting 33.8 million transactions, amounting to Rs. 2.4 trillion, which translates to a strong 13.9 percent progress in terms of volume and a 28 percent increase in the value of these transactions compared to the preceding quarter.

The retail sector also continued its upswing in the adoption of digital payments. During the quarter, a total of 31.4 million transactions amounting to Rs. 178.1 billion were processed via 92,153 Point-of-Sale (POS) terminals. This shows an impressive double-digit QoQ growth of 11.8 percent by volume and 32.1 percent by value. Similarly, the number of e-Commerce merchants also increased by 32.6 percent reaching a total of 3,968. The onboarding of QR merchants largely added to this growth. These merchants processed 13.6 million transactions worth Rs. 26.7 billion, showing QoQ growth of 7.2 percent by volume and 19.8 percent by value.

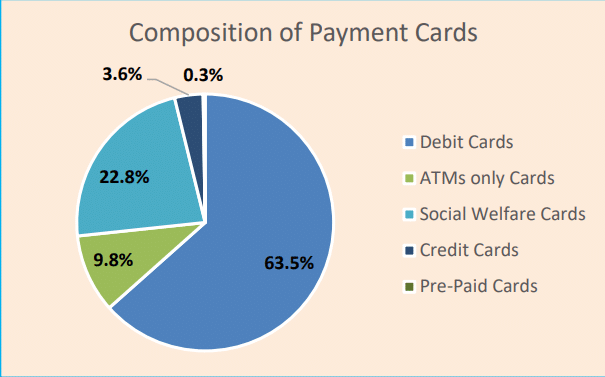

As of end-December 2022, there were 5.4 percent more cards than in the preceding quarter, reaching 48.6 million cards in circulation which mainly comprised of Debit Cards (63.5 percent), Social Welfare Cards (22.8 percent), ATM only Cards (9.9 percent), Credit Cards (3.6 percent), and Prepaid Cards (0.3 percent).

During this quarter, paper-based transactions showed relatively slower growth of 3.4 percent in volume and 12.2 percent in value on a QoQ basis. In the Large-value (wholesale) payments segment, SBP’s Real-time Inter-Bank Settlement Mechanism (PRISM) processed a total of 1.1 million transactions amounting to Rs. 161.3 trillion, showing QoQ growth of 5.9 percent in volume and 1.4 percent in value.

Two EMIs, namely M/s Finja and M/s Nayapay, have also continued to strengthen their presence in the domestic payments landscape. The nontraditional fintechs of this sort are poised to take the advantage of increasing digital adoption by the customers. As more such players enter the market, the objective of improving financial inclusion will also increasingly materialize. This shift to digitalization was already happening even before the pandemic arrived. However, by the sheer force of necessity, the pandemic accelerated this change, and the data indicates that this trend is sticking.

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.