Writing Checks – An Extensive Financial Guide

Learn how to write a check by reading the guide below.

Table of Contents

(The articles will be placed in the particular order)

- How to Write a Check – Usage of Checks in Organizations and Banking

- The ‘WHAT IS’

- Check – Writing

- Electronic Check Processing

- Out-dated Checks – rejection

- Post-dated Checks

- Will the Check Clear?

- A Simple Instruction – Fill your Check

- Record Payment in Check Register

- MODUS OPERANDI – Rest Assured

- Types of Checks – Pay Attention!

- Check Fraud Prevention Measures

- Tips on how to protect your checks from being used fraudulently

- How to protect yourself from fraudulent checks given to you

- Additional Helpful Tips

- Security Tips

- Play it Safe

- FAQs – Don’t blame the System

- Why do Checks Bounce?

- Are cheques only valid for 6 months?

- Special Limitations?

- Paid Cash – Check still Bounced. WHY?

- Advice to anyone inconvenienced by time-delay to access check funds

- Other Financial Instruments

- o Loans and Bonds

- o Asset-Backed Securities

- o Stocks

- o Funds

- o Options and Futures

- o Currency

- o Swaps

- o Insurance

How to Write a Check – Usage of Checks in Organizations and Banking

Presently, the banking industry has become more competitive than ever. They continue to establish and promote new financial instruments throughout the commercial and corporate banking sectors of the world. So much so that the old ways are in danger of going obsolete.

Although they’re a lot less common as they once were, checks are still widely used throughout the world. They’re an inexpensive and effective tool for moving money and prove to be quite safe when it comes to a range of transactions. But what exactly is a check and how would a first-timer like me use it?

The What Is?

Checks are official instruments or documents that order a bank to pay or transfer money to a specific payee. It’s a two-way street; the name of the payee mentioned on the check, receives money from the bank account of the payer who, evidently, issued the check in the first place. Let’s look thoroughly at the components of this definition. First of all, the payee is the beneficiary of the transaction, who can receive the mentioned amount of cash using check or can deposit the mentioned amount of money directly into his/her account.

The payer is someone who issues a check against services that he/she received from the payee. In order to use checks, however, you need to have a bank account. A bank account is a financial account maintained by a financial institution that governs it. In terms of banking systems, a check book is issued upon request of the customer and is either hand-delivered to them at the location provided, or the customer receives it directly by visiting the bank.

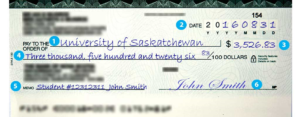

Let’s first review what a check is, and what content appears on it.

- Date: The date is written on the top right-hand corner of the check. A check has to be presented to the bank within six months of the mentioned date on the check. If not, the check will be a stale check and it will be dishonoured.

- The Drawee: This is the bank on which the check is drawn. This is printed on the check and helps when queries arise.

- The Branch Code Number: This appears on the top right-hand corner and at the bottom of the check.

- The Payee’s Name: This is written on the top line of the check.

- Amount: The amount should be written in words and in figures. The amounts should be the same. If not, the check will be dishonoured.

- The Drawer’s Name: This is printed or written at the bottom of the check.

- The Drawer’s Signature: The drawer’s signature should appear below the drawer’s name. If the signature is not the same as the specimen signature given to the bank, the check will be dishonoured.

- The Check Number: This appears at the bottom left hand corner of the check.

The Account Number: The account number also appears at the bottom of the check. This helps in the automatic handling of checks.

Now, writing checks is simple and safe. All you need is to get the basics.

Check Writing

In this easy and simple task, you have to:

- Write the name of the person or organisation you’re paying

- Draw a line through any blank spaces on the check so people can’t add extra numbers or names

- Add details (such as a reference or account number) to the payee line. This makes sure the money ends up in the right place

- Keep the check stub that contains the details and reference

- Make sure you have enough money in your account to cover the value of the check until the person has paid it in and the money has been deducted. If you don’t, some banks might charge you a fee for the bounced payment.

Electronic Check Processing

In the present age, some banks allow you to use their online banking applications – most commonly through smartphone apps – to pay in a check by taking a photo of the physical check. Then the procedure prompts user to fill some details pertaining to it. Typically, it takes a day for the check to clear but the procedure gets longer over weekends or due to public holidays. But when does money leave or enter your associated bank account?

- When you write a check, the money usually leaves your account three working days after the person pays in your check.

- When you pay in a check, you’ll be able to use the money four working days later – but you won’t be sure the check has cleared (the money is really yours) until six working days after you’ve paid it in. If you use the money in the meantime, you might have to pay it back.

- If you used check imaging to pay in your check, the money will be available within two working days, and often the next working day.

It is true that checks do not have expiration dates, but they often get rejected if dated more than 6 months or earlier. This aspect primarily depends on the bank’s policies.

Out-dated Checks – Rejection

As mentioned earlier, old checks tend to get rejected by banks because this brings into question the validity of the piece of paper. To avoid such problems, make sure you:

- Pay in all checks you’re given as soon as possible.

- If someone you’ve paid asks you for another check, saying they’ve lost the original or that it’s gone out of date – ask your bank to stop the previous check first! You wouldn’t want to lose double the money for half of what you paid for.

Post-dated Checks

Do NOT accept post-dated checks. If you pay in a post-dated check then it might be returned as unpaid. Although there’s a future pay-in date associated with this procedure, but it is highly risky and tends to create problems – more than you already might be having.

Will the check clear?

If a person is writing a check without having sufficient money, or is committing fraud, then the check will ‘bounce’. The payee won’t get money. In this case, he’ll need to ask for a ‘special presentation’. His bank will send the check to the bank which issued the check, by first class post, and phone them the next day to confirm that it will be paid.

Of course there’d be some compensation that the bank will earn because of this, but complications get removed. It is fairly simple: You won’t get the money any quicker, but you’ll find out if you’ll eventually get paid or not.

A Simple Instruction | Fill Your Check

There can only be one way to write the perfect check. Let’s go through the steps:

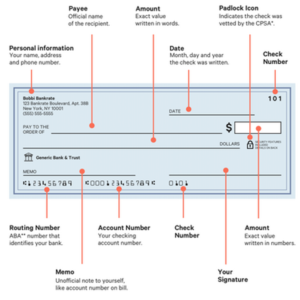

- Payee: On the line that says “Pay to the order of,” write the name of the person or organization you’re paying. You may have to ask “Who do I make the check out to? if you’re not sure what to write, because this information needs to be accurate.

- Current date: Write this near the top right-hand corner. In most cases, you’ll use today’s date, which helps you and the recipient keep accurate records. You can also postdate the check, but that doesn’t always work the way you think it will.

- Amount in numeric form: Write the amount of your payment in the small box on the right-hand side. Start writing as far over to the left as possible. If your payment is for $8.15, the “8” should be right up against the left-hand border of the dollar box to prevent fraud. See examples of how to write in the amount.

- Amount in words: Write out the amount using words to avoid fraud and confusion. This will be the official amount of your payment. If that amount is different from the numeric form that you entered in the previous step, the amount you wrote with words will legally be the amount of your check. Use all capital letters, which are harder to alter.

- Memo (or “For”) line: If you like, include a note. This step is optional and will not affect how banks process your check. The memo line is a good place to add a reminder about why you wrote the check. It might also be the place to write information that your payee will use to process your payment (or find your account if anything gets misplaced). For example, you could write your Social Security Number on this line when paying the IRS, or an account number for utility payments.

- Signature: Sign the check legibly on the line in the bottom-right corner. Use the same name and signature on file at your bank. This step is essential—a check will not be valid without a signature.

Below is a check to telly instructions 1-6

Keep it in mind to record each check you write on the stub in the checkbook. Check this info against your statement and report problems to the bank if you see any.

After writing the check, may want to keep a record of your payment. A check register is ideal whether you use an electronic or paper register. Recording payments prevent you from spending the same amount of money twice because get this: the funds will still show as available in your account until the check gets cleared. This may take a while, so make the note of payment with a fresh mind!

Before writing the check, however, make sure that it is something you really need to do. Writing a check can be problematic, and it isn’t the fastest mode to transfer cash. You may have other options like:

- Paying bills online, and even tell your bank to send a check automatically each month. You won’t need to write the check, pay for postage, or get the check in the mail

- Getting a debit card and spending with that instead. You’ll pay out of the same account, but you’ll do it electronically. There’s no need to use up checks (which you’ll have to re-order), and you’ll have an electronic record of your transaction with the payee name, the date of your payment, and the amount

- Setting up automatic payments for regular payments like utility bills and insurance premiums. There’s typically no charge to pay this way, and it makes your life easy. Just be sure that you’ve always got enough cash in your account to cover the bill

Caution: No matter what method you use to pay, make sure you always have sufficient funds available in your bank account. The check might bounce and create problems if you don’t!

Record Payment in Check Register

Make a note of the transaction in your check register. Copy everything from your check so you know what happened later. Calculate your running balance so you know how much money you have right now. Justin Pritchard

Make a record of every check you write in a check register. Doing so will allow you to:

- Track your spending so you don’t bounce checks

- Know where your money goes. Your bank statement may only show a check number and amount—with no description of who you wrote the check to

- Detect fraud and identity theft in your checking account

You should have received a check register when you got your check book. If you don’t have one, it’s easy to make your own using paper or a spreadsheet.

Copy all of the essential information from your check:

- The check number

- The date that you wrote the check

- A description of the transaction or who you wrote the check to

- How much the payment was for

If you need more details on where to find this information, see a diagram showing the different parts of a check.

You can use your register to balance your checking account. This is the practice of double-checking every transaction in your bank account to make sure you and the bank are on the same page. You’ll know if there are mistakes in your account, and if anybody has failed to deposit a check you wrote them (thereby making you believe you have more money to spend).

Your check register can also provide an instant view of how much money you have available. Once you write a check, you should assume that the money is gone—in some cases, the funds are drawn from your account quickly because your check is converted to an electronic check. That feels fast, right?

Modus Operandi – Rest Assured

Checks are no longer a popular method of payment as they once were some years ago as banking has evolved and advanced, and has become digital. In the event that you receive a check or have the need to use one, please take note of the tips below.

- Check the payee, amount in words and figures carefully for alterations

- Be on the lookout for stamps that are placed over areas that could conceal alterations

- Checks issued in thick black pen should raise suspicion

- Lookout for spelling mistakes on the printed areas of the checks such as the drawer’s details and the Bank branch name

- Check for tampering on the line where codes are written – black shaded areas

- Be suspicious if the check appears faded, as chemicals could have been used to remove information

- A shaky signature could indicate that the signature was traced

- Treat typed or pre-issued checks with caution

- Write your check in such a way that it is difficult to alter

- Write clearly and neatly using a non-erasable ballpoint pen. The type of pen you use makes a difference. Most ballpoint and marker inks are dye based, meaning that the pigments are dissolved in the ink. But, based on ink security studies, gel pens, like the Uni-ball 207 uses gel ink that contains tiny particles of colour that are trapped into the paper, making check washing a lot more difficult

- Write the full names of the payee and spell them correctly. Avoid abbreviations

- Do not make any corrections to the check as alterations in any form will not be allowed on the check except for where the words “bearer/order” has been ruled through. It is best to cancel it and write out another one

- Don’t leave large spaces between words and draw a line through any unused space to ensure that nothing can be added to the check

- Fill in the correct date

- Remember to sign your check

What else can you do to keep your checks safe?

- Keep your checkbook, cancelled checks, and statements safe

- Never sign a blank check

- Report lost or stolen checks immediately

- Provide your Bank with up-to-date signatures of everyone who is entitled to sign checks on your account

- Check your statements every month and do reconciliation

- It is safest to collect your new checkbook yourself

The way you make your check payable can protect you:

- A ‘cash’ check is as good as money so it is not your safest option

- Checks where the words ‘Or Bearer’ are not crossed out are as good as cash and can be cashed by anyone who presents it (even if it was made out to a person or company). If you do not want the check to be negotiated between various parties, you can restrict negotiation by adding the words “Not Transferable”. This in effect means that the check may only be negotiated by the person/company whose name appears on the beneficiary field

- When a check is made out to a person or company and ‘Or Bearer’ is crossed out, it is safer. However, the original payee can still sign the back of the check and make it over to a third party

How does crossing your check protect you?

- Two lines with or without the words ‘non-negotiable’ or ‘non-transferable’ written between them means the check cannot be cashed but must be deposited into a bank account

- A crossing cannot be cancelled

- ‘Non-transferable’ means it must be paid into the account of the person or company whose name appears on the check

- ‘Non-negotiable’ means it must be paid into a bank account but the person to whom the check was originally made out to may transfer it to a third party.

- It is not advisable to post a check

- If you must send it via post, make sure checks are crossed, marked non-transferable’ and made payable to a specific person or company

- Send checks by registered mail and in good time to allow for delivery delays

- Staples or paperclips attaching a check to a letter are all tell-tale signs for criminals

- Avoid envelopes that are transparent or easy to open

When accepting a check make sure that:

- It has not been altered

- It isn’t post-dated

- It is signed

- There are no dirty marks on it

- The same pen has been used throughout

- The handwriting is the same on all parts of the check

Be cautious when you notice the following on a check:

- Several stamps that are placed over areas that could conceal alterations

- Thick black pens or markers used to complete the check

- Spelling mistakes on the printed areas such as the drawer’s details and the Bank Branch name

- Tampering or black shaded areas on the branded code-line

- Faded areas, as chemicals could have been used to remove information

Points to Remember

- When accepting a bank-guaranteed or bank-issued check, remember that the issuer might give you this check, wait for you to release the goods and then quickly cancel the check for some fictitious reason.

- When accepting a check, don’t release goods until the funds have been paid into your account or request a special clearance from the bank on the check deposit in question.

Types of Checks – Pay Attention

1) Bearer Check

A check is called bearer check when the “bearer” written on the right of the check is not cancelled or marked. The term “Bearer” mentioned on the check means that the one whoever is in the possession of the check can withdraw it. Therefore, these types of checks are risky in nature. If a bearer check is lost, it can be encashed by the person who finds it. Therefore, it is the same as cash in nature and is advised to be handled carefully, because banks don’t verify the identity of the person. There is no need to mention the name of the payee on a bearer check or “Pay to the order of cash” can be written at the place of payee’s name.

2) Order check

A check is called order check when the “bearer” written on the check is cancelled or marked. This check can be encashed by the person whose name is mentioned on the check. In a few circumstances, the check can be encashed by some other person / endorsed by the receiver if “or order” is mentioned alongside the name of the payee.

3) Crossed check

A check is called crossed check when two parallel lines are drawn on the top left corner or top right corner of the check. Additional words like “& CO.” or “Account Payee” or “Not Negotiable” can also be mentioned along with two parallel lines. This check cannot be encashed on the bank’s counter.

It can only be deposited in the bank account of the payee. Therefore, these types of checks are considered the safest types of checks. A payee must have a bank account to encash crossed check and it is advisable to write the same name as payee has on his or her bank’s passbook. In case of wrong spellings or unreadable handwriting, the check will not be accepted by the bank.

4) Uncrossed or open check

A check is called crossed check when it is not crossed by drawing two parallel lines on it. Cash can be obtained on the bank’s counter by using this type of check. This type of check can be bearer or order check.

5) Anti-dated check

A check is called anti – dated check when an earlier date is mentioned on the check than the date it is brought to the bank. These types of checks remain valid for the duration of 3 months, after which they become invalid and cannot be encashed. Therefore, it is important to write the correct date on the check and encash it before the duration of three months.

6) Post – dated check

A check is called post-dated check when the date mentioned on it is yet to come. These types of checks are issued on mutual agreement of payer and payee. However, these types of checks cannot be paid before the date written on the check. It can only be paid on or after (up to three months) the date mentioned on the check. It is advised to check the date written on the check before accepting it from the payer. It is used very commonly in businesses as a Post-dated check can be taken as collateral.

7) Stale check

A check is called stale check when it is presented to the bank after the three months of duration. Any check remains valid up to three months of duration. A bank does not credit a stale check.

8) Mutilated check

A check is called mutilated check if it is torn in two or more pieces. Usually, a bank does not accept mutilated checks. However, in some special circumstances (when the check is mildly torn), the bank needs confirmation from the payer before crediting these types of checks.

It is mandatory to maintain sufficient balance in the bank account, at least the amount of the check to be deposited. For example, your bank balance is $100 and you have written a check of $90 to someone. The person can easily withdraw the $90.

But if you have only $89 in your bank account, then the check will not get cleared and the phenomenon is called Check Bounce. Frequent Check bounce can hamper your financial credibility.

Check Fraud Prevention Measures

It might sound ironic that we are talking about check fraud in an era of high technology and instantaneous payments, but this problem is very real, even in today’s world. Check fraud can take several forms — counterfeit/fake checks, altering beneficiary details fraudulently or genuine check with a forged signature. In this article, we will mainly focus on the first problem of counterfeit or fake checks.

Check fraud can happen a few different ways. Criminals can steal checks, create fraudulent checks or change the name or amount of a legitimate check. In any case, there are a number of steps that you can take to protect yourself from check fraud.

Incidents involving fake checks occur with regularity, while banks and regulators keep updating the security features and specifications to identify genuine checks. With advancements in technology, even fraudsters have upped the ante. Hence, there have been increasing cases in recent times which have not been detected through the regular scrutiny and processing and have therefore resulted in significant monetary losses for the banks and account holders. Although it may appear on the surface to be a minor issue, it has already resulted in a hit to the bottom line and in some instances, even eroded the credibility of the bank and the banking system at large.

Fun Fact: While the use of checks has been declining with the growing popularity of electronic and card payments, financial institutions still process nearly one billion checks every year.

Tips on How to Protect Your Checks being used Fraudulently

- Keep your checks in a secure location.

- Review your monthly bank statement or regularly check your transactions through online or telephone banking. If you see transactions you didn’t do, notify your bank immediately and they will investigate.

- If you close your account, shred any unused checks.

- Consider electronic payments such as wire payments, direct deposit of payments, pre-authorized payments for bills or email money transfers as they are more secure than checks.

How to protect yourself from fraudulent checks given to you

There are a number of security features built into checks to help prevent fraud. Banks will try to detect fraudulent checks, but it isn’t always possible to do so until it goes through the check clearing system. Here are some tips on how to spot a fraudulent check yourself:

How to Detect a Fraudulent Check

- Details about the security features that are built into checks are usually printed on the back of the check and can include things such as watermarks and intricate designs that will disappear if the check is scanned or photocopied.

- If you have accepted a check as payment for something you are selling, know who you’re dealing with and whenever possible, make sure that the check, money order or bank draft has cleared and that the money has been confirmed before you release the item to the buyer. This step is highly critical. This ought to be sorted out in advance when the buyer first reaches you about the thing.

- For worldwide transaction, it could be longer. In case you’re feeling uneasy about the exchange in any way, shape or form or on the off chance that you are suspicious about anything, don’t proceed with it. Losing the sale is better than losing your money on charges of fraudulent financial practices.

- For money orders and bank drafts, if you are suspicious, you can have your bank call the check writer’s bank to confirm authenticity.

-

- Consider switching to electronic forms of payment such as wire transfers or e-mail money transfers, particularly if you don’t know the check writer. Electronic payment is more secure than checks.

Remember, you are responsible for all the checks deposited into your account. While your bank may provide you with provisional credit, giving you access to the funds right away when you deposit a check, the provisional credit will be removed from your account if the check is found to be fraudulent when it is processed. This could happen in a few days or significantly longer if the check is written on a foreign bank account. It is then your responsibility to get payment from the person or organization that owes you money.

Additional Helpful Tips

- Make sure any checks that you write or accept from others are properly dated and completed.

- Don’t accept checks showing any signs of alteration.

- Don’t accept post-dated checks and never agree to hold a check until a future date.

- Don’t accept a check made out to another individual and then signed over to you.

- If you are selling something, don’t accept checks for an amount greater than the purchase price. This is a common scam known as an Overpayment Scam.

- Keep in mind that legitimate business checks can sometimes be altered and used as a payment. Before accepting a business check, ask yourself if it makes sense that a check be drawn on a business account or that of a large corporation.

- Don’t accept counter checks (checks with no pre-printed information such as name, address, or account number).

PLUSSSS…

Check fraud is a billion-dollar problem. Check fraud victims include banks, businesses and consumers. Our current system for cashing checks is somewhat flawed. Checks can be cashed and merchandise can be purchased even when there is no money in the checking account.

There are 5 main forms of check fraud to watch out for:

Forged signatures are the easiest form of check fraud. These are legitimate checks with a forged signature. This can occur when a check book is lost or stolen, or when a home or business is burglarized. An individual who is invited into your home or business can rip a single check from your check book and pay themselves as much as they like. Banks don’t often verify signatures until a problem arises that requires them to assign liability.

Forged endorsements generally occur when someone steals a check written to someone else, forges endorsement and cashes or deposits it.

Counterfeit checks can be created by anyone with a desktop scanner and printer. They simply create a check and make it out to themselves.

Check kiting or check floating usually involves two bank accounts, where money is transferred back and forth, so that they appear to contain a balance which can then be withdrawn. A check is deposited in one account, then cash is withdrawn despite the lack of sufficient funds to cover the check.

Check washing involves altering a legitimate check, changing the name of the payee and often increasing the amount. This is the sneakiest form of check fraud. When checks or tax-related documents are stolen, either from the mail or by other means, the ink can be erased using common household chemicals such as nail polish remover. This allows the thieves to endorse checks to themselves.

Uni-ball pens contain specially formulated gel ink that is absorbed into the paper’s fibers and can never be washed out. The pen costs two bucks and is available at any office supply store.

Consider:

- A locked mailbox so nobody can access your bank statements.

- Using online banking and discontinuing paper statements.

- Never toss old checks in the rubbish, always shred them.

- Have checks delivered to the bank for pick up opposed to your home.

- Guard your checks in your home or office, lock them up.

- Go over your bank statements carefully.

Security Tips

Develop the habits below to decrease the chances of fraud hitting your account.

- Make it permanent: Use a pen whenever you write a check. If you use a pencil, anybody with an eraser can change the amount of your check and the name of the payee.

- Keep your check book in a secure place.

- Don’t sign an incomplete or blank check.

- It’s important to ensure the check can only be banked by the person or company it’s intended for. To do this, write the words ‘Not transferable’ or ‘A/C payee only’ or ‘Account payee only’ within two parallel lines cross across the face of the check. Make sure you know the correct payee name.

- You can write the words ‘Not negotiable’ within two parallel lines across the face of the check. This means the check must be paid into a bank account. A check marked ‘not negotiable’ can be transferred to someone other than the person it is made out to, but it still has to be paid into a bank account.

- When writing the check amount in words, begin writing as far possible to the left of the space provided and add the word ‘only’ after the amount. This ensures that other words and figures can’t be added.

- Draw a line through any unused portion of the payee or amount spaces, so that there’s no unwritten space.

- If you make an alteration to something you have written, confirm by signing your full signature alongside the alteration.

- If you change your postal address, let your bank know immediately

- No blank checks: Don’t sign a check until after you’ve filled in the name of the payee and the amount. If you’re not sure who to make the check payable or how much something costs, just bring a pen—it’s much less risky than giving somebody unlimited access to your checking account.

- Keep checks from growing: When you’re filling in the dollar amount, make sure you print the value in a way that prevents scammers from adding to it. Do this by starting at the far-left edge of the space, and draw a line after the last digit. For example, if your check is for $8.15, put the “8” as far to the left as possible. Then, draw a line from the right side of the “5” to the end of the space or write the numbers so large that it’s hard to add any numbers. If you leave space, somebody can add digits, and your check might end up being $98.15 or $8,159.

- Carbon copies: If you want a paper record of every check you write, get check-books with carbon copies. Those check-books feature a thin sheet containing a copy of every check you write. As a result, you can quickly identify where your money went and exactly what you wrote on every check.

- Consistent signature: Many people don’t have a legible signature, and some even sign checks and credit card slips with complicated scribbles. But consistently using the same signature helps you and your bank identify fraud. It’ll be easier for you to prove that you’re not responsible for charges if a signature doesn’t match.

- No “Cash”: Avoid writing a check payable to cash. This is just as risky as carrying around a signed blank check or a wad of cash. If you need cash, withdraw from an ATM, buy a stick of gum and get cash back using your debit card, or just get cash from a teller.

- Write fewer checks: Checks aren’t exactly risky, but there are safer ways to pay for things. When you make electronic payments, there’s no paper to get lost or stolen. Most checks get converted to an electronic payment anyway, so you’re not avoiding technology by using checks. Electronic payments are typically easier to track because they’re already in a searchable format with a timestamp and the name of the payee. Use tools like online bill payment for your recurring expenses, and use a credit or debit card for everyday spending.

Play it Safe

There are some key basic rules to follow.

-

Why do Checks Bounce?

The typical reason for a bank to bounce a check is either because a customer does not have enough money in their account to pay the check, or they have used all of their overdraft facility. In addition, when a bank spots a fraudulent check it will bounce it. But banks also bounce checks because: the checks have not been signed correctly (e.g. one signature when two are required) or perhaps not signed at all; because they are more than six months old or post-dated; or corrections have not been signed or initialled; or because the amount in words differs from the amount in writing. The vast majority of checks are paid and do not bounce. Only around 0.5% of all checks are returned unpaid each day.

If your check bounces, you’d be asked to pay a penalty. To be on the safe side, repay the amount immediately to avoid any legal proceedings that may disturb your timeline.

-

Are cheques only valid for 6 months?

No. A check is valid for as long as the debt between the two parties (i.e. the person writing the check and the person they give it to) exists. In other words, checks don’t have an expiry date. However, it is common banking practice to reject checks that are over six months old to protect the person who has written the check, in case the payment has been made another way or the check has been lost or stolen. This six-month timeframe is at the discretion of banks involved – and in general as well. It should not be assumed that checks older than six months would automatically be rejected as the only definite way to cancel a check is for the person who wrote it to request that a stop be placed on it.

If you have a check that you want to pay in that is more than six months old, your best course of action is to not pay it in and instead obtain a replacement from the person who gave it to you. Where there is a dispute, a check remains legally valid in order to provide proof of the existence of a debt for a period of six years, which is the Statute of Limitations.

Special Limitations?

In the old days, when checks took six days to clear, if you received a check and you wanted to know as soon as possible whether it would be paid, you could ask your bank to present that check ‘specially’. The bank then sent the check by first-class post directly to the payer’s bank, contacting them by phone on the following weekday to confirm whether it would be paid. Banks call this “certainty of fate”.

However, with the advent of check imaging, the quicker clearing timescale typically provides certainty of fate at the end of the next weekday after paying a check into a bank account, so customers are much less likely to need a check to be specially presented. Because of this, fewer banks will be offering this service and it may not be for all checks that are paid in so you will need to talk to your bank to find out more.

Paid Cash – Check still Bounced. WHY?

This situation may arise if you pay the cash into your account via a bank other than your own. As your cash deposit is typically accompanied by a paying-in slip, this piece of paper has to be turned into to a digital payment message that goes through the Image Clearing System, which means the deposit will get to your bank and into your account by 23.59 the next weekday after you paid the cash in. Punctuality is a foundational code of ethics!

Cash paid into your own bank will be credited to your account on the same day, provided you paid it a weekday before the bank’s advertised cut-off time.

Advice to anyone inconvenienced by time-delay to access check funds

You should make sure that you’ve got an account which perfectly fits your needs. If quicker access to check funds is vital, you ought to go searching for an account which offers more favourable terms. Some accounts allow early access to funds from a check, sometimes not as. Remember, it varies from bank to bank. However, you should be aware that the funds aren’t definitely yours to keep until the end of the sixth working day after paying the check in. If you withdraw the funds and the check is then returned unpaid (i.e. bounces) before the end of the sixth working day, in most cases the bank will ask you to give the money back.

Anyone who needs a quicker way to pay or receive money should use an online, mobile or telephone banking payment, which can typically be made in a few minutes. Search about QR-based banking solutions on the web. If your bank offers any one of them, then it may suit you greatly.

Other Financial Instruments

There are many types of financial instruments. Many instruments are custom agreements that the parties tailor to their own needs. However, many financial instruments are based on standardized contracts that have predetermined characteristics. Read further to understand.

Some of the most common examples of financial instruments include the following:

- Exchanges of money for future interest payments and repayment of principal.

- Loans and Bonds. A lender gives money to a borrower in exchange for regular payments of interest and principal. It is a simple no-risk process that may involve an interest percentage added to repayment.

- Asset-Backed Securities. Lenders pool their loans together and sell them to investors. The lenders receive an immediate lump-sum payment and the investors receive the payments of interest and principal from the underlying loan pool.

- Exchanges of money for possible capital gains or interest.

- Stocks. A company sells ownership interests in the form of stock to buyers of the stock.

- Funds. Includes mutual funds, exchange-traded funds, real estate investment trusts, hedge funds, and many other funds. The fund buys other securities earning interest and capital gains which increases the share price of the fund. Investors of the fund may also receive interest payments.

- Exchanges of money for possible capital gains or to offset risk.

- Options and Futures. Options and futures are bought and sold either for capital gains or to limit risk. For instance, the holder of XYZ stock may buy a put, which gives the holder of the put the right to sell XYZ stock for a specific price, called the strike price. Hence, the put increases in value as the underlying stock declines. The seller of the put receives money, called the premium, for the promise to buy XYZ stock at the strike price before the expiration date if the put buyer exercises her rights. The put seller, of course, hopes that the stock stays above the strike price so that the put expires worthless. In this case, the put seller gets to keep the premium as a capital gain.

- Currency. Currency trading, likewise, is done for capital gains or to offset risk. It can also be used to earn interest, as is done in the carry trade. For instance, if a trader believed that the Euro was going to decline with respect to the United States dollar, then he could buy dollars with Euros, which is the same thing as selling Euros for dollars. If the Euro does decline with respect to the dollar, then the trader can close the position by buying more Euros with the dollars received in the opening trade. If all regulations are kept intact, this procedure runs smoothly – without human error.

- Swaps. Swaps are an exchange of interest rate payments calculated as a percentage of a notional principal that is paid at periodic intervals. One leg of the swap pays a fixed rate of interest and the other leg pays a floating rate of interest. However, only the net amount is exchanged.

For instance, if the interest based on the floating rate is $1000 greater than the interest based on the fixed-rate on a payment date, then the party receiving the fixed rate would pay $1000 to the party receiving the floating rate. The receiver of the fixed rate of interest enters into the swap usually to offset risk while the receiver of the floating rate generally hopes to profit from changes in the market interest rate. Usually, the floating rate is calculated as a spread above LIBOR (a benchmark interest rate) or some other benchmark, such as Treasuries with comparable terms. If both legs of the swap pay in the same currency, and the swap is known as an interest rate swap, since both the fixed-rate and the floating rate are paid in the same currency. By contrast, a currency swap is the exchange of interest rate payments paid in different currencies, so the net amount is calculated based on the exchange rate on the payment date.

- Exchanges of money for protection against risk.

- Insurance. Insurance contracts promise to pay for a loss event in exchange for a premium. For instance, a car owner buys car insurance so that he will be compensated for a financial loss that occurs as the result of an accident.

Insurance varies with specific services for a specific contract. In the above example, you may add life insurance – a premium for life (and a bit sensitive, so let’s not discuss this in detail here).

Concluding Verdict

Issuing a payer’s check, evading fraudulent circumstances, and being content-conscious is all part of a perfectly symmetrical triangle. You need to have a near-accurate degree of understanding basic banking practices, otherwise the triangle won’t look symmetrical – your money won’t be safe, just saying.

This article provides an extensive study about checks and different types of financial practices moulded into an instrument. All concepts mentioned represent important pillars of the financial institution groups – FIGs – that we heavily trust our money with. The facts directly compliment views and opinions of experts and we recommend that you see what they are trying to ‘preach’.

You don’t have to memorize the theory but strengthen your aspect of financial literacy to the point where writing a simple check wouldn’t turn into an unwanted nuisance. Play it safe – learn, then act accordingly!