The State Bank of Pakistan (SBP) has notified the Rules for Investment in ‘Naya Pakistan Certificates’ that are issued by the government to attract investments from overseas Pakistanis to boost foreign exchange reserves of the country.

SBP stated that the eligible individuals will place the order to subscribe to the certificates electronically by visiting the Naya Pakistan Certificate webpage of their respective agent bank and giving investment details including currency, tenor, and the amount they wish to invest. The eight agent banks are Habib Bank Limited (HBL), United Bank Limited (UBL), Meezan Bank, Bank Alfalah, MCB Bank, Faysal Bank, Samba Bank, and Standard Chartered Bank.

These certificates would be subscribed through Foreign Currency Value Account (FCVA) or NRP [Non-Resident Pakistani] Rupee Value Account (NRVA), being marketed as Roshan Digital Accounts (RDAs) by the agent banks, the SBP said.

The funds for investment in certificates must be remitted from abroad in the investor’s FCVA or NRVA after June 30, 2020. The agent banks shall be responsible for Know Your Customer (KYC), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD) of the investors.

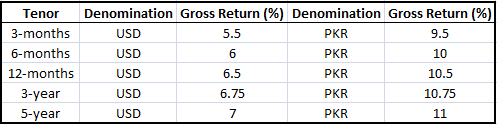

The denomination will be in both USD and PKR, thus, investors shall have the option to subscribe either PKR denominated or US Dollar-denominated certificates of 3-Month, 6-Month, 12-Month, 3-Year, and 5-Year tenors.

The eligible investors would need to make a minimum investment of $5,000 with integral multiples of $1,000 in dollar-denominated certificates, while for the Rupee denominated certificates, the minimum amount will be Rs. 100,000 with integral multiples of Rs. 10,000.

The 3-Month, 6-Month, and 12-Month tenor certificates shall be single-coupon securities on which principal and profit shall be paid on maturity or on premature encashment. Whereas, 3-year and 5-year certificates shall be coupon securities, on which periodic profit payment shall be paid on a half-yearly basis.

The periodic coupon payments would be made on a six-monthly basis only for certificates of 3-year and 5-year maturities in their respective currencies.

The investors can have premature encashment of their certificates. Premature encashment proceeds would be worked out such that the rate of return accruing to that investor is equivalent to the rate of return of the nearest shorter maturity of certificates or such rate as may be notified by the finance division from time to time. No profit will be paid in case of encashment of certificates before the completion of three months.

Maturity proceeds of certificates, including the amount of final coupon (net of deduction of tax), would be credited to the dollar clearing account or rupee current account of the investor’s bank account maintained with the SBP.

On realization of maturity proceeds by the banks in their accounts with the SBP, the bank would be liable to credit the FCVA or NRVA of the respective investor on the same day, failing which the bank would be liable to make the investor good by paying compensation for the delayed period at the coupon rate as may be applicable to the respective certificates.

The agent banks shall, after debiting the investor’s account with an amount equal to the amount of his/her investment order, consolidate the orders received from FCVA or NRVA holders during a working day till 1:00 p.m. Pakistan Standard Time (PST), and shall transmit the same on the prescribed format to the SBP through SBP’s Data Acquisition Portal (DAP) by 2:30 p.m. (PST) the same day.

In case of purchase of USD denominated certificates, agent banks have two options to remit the purchase value of certificates to the State Bank of Pakistan (SBP) either through their USD Clearing Account maintained with SBP, or through a transfer of funds to the Nostro account of SBP maintained with the Federal Reserve Bank of New York, New York, USA.

Transaction charges, including but not limited to correspondent bank charges shall be on the account of the banks, and the banks shall ensure to remit to the SBP Nostro account the complete purchase amount of the Certificates.

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.

I want to ask that, profit you will be earning in this regards, is that the interest you are taking from the bank ? Is that the Halal for Muslim to do that ?

This certificate is based on loan transaction (guaranteed principal) with interest payment promised.

By virtue of promised return on loan it becomes riba. And hence is forbidden in Islam.

An easy, viable, halal alternative is making these certificates on basis of partnership or mudarbah. This product is already available with Islamic banks worldwide.

what about Naya Pakistan Certificates is Halal or not?

Has Meezan bank come up with alternate Islamic instrument for Naya Pakistan Certificates?