In recent weeks the fear that has gripped the financial markets and different stakeholders of the economy is that if prudent and timely economic measures are not taken, Pakistan may spiral out of control, much like Sri Lanka.

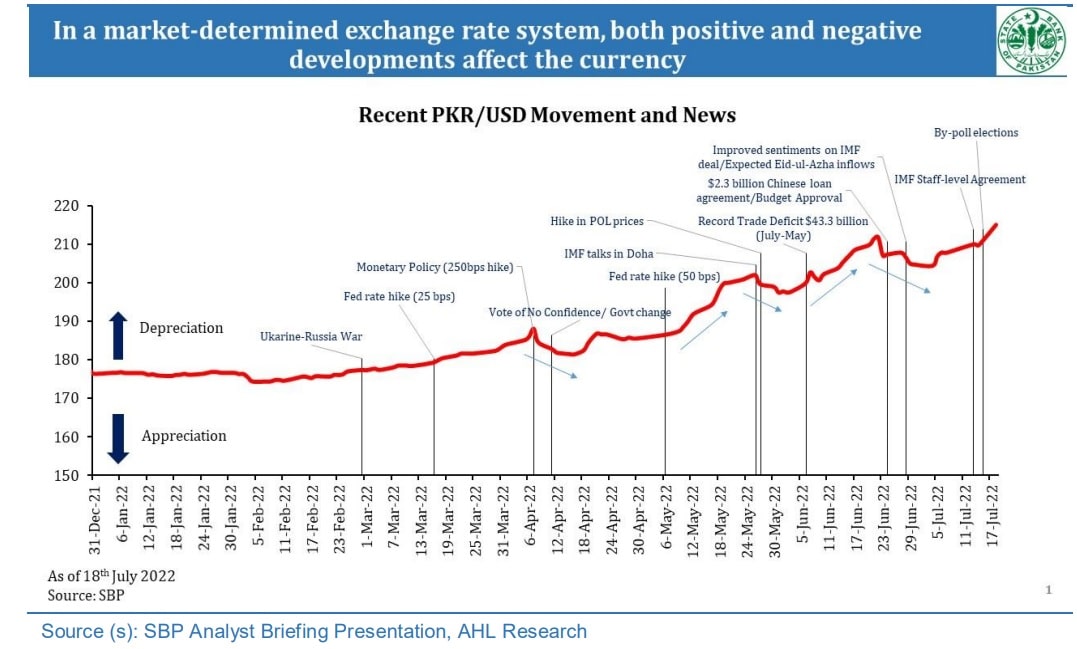

This accelerated the free fall of the Pakistani Rupee (PKR) against the US Dollar (USD) in the interbank recently. However, according to a report by Arif Habib Ltd the initial major depreciation of PKR against the USD was triggered back in April, post the vote of no-confidence (VoNC) leading to political change in the country.

The political risks and shifting paradigms took a toll on the foreign investors and creditors confidence, hence contributing largely to bringing the PKR under pressure. In the last few weeks, the PKR witnessed a free fall against the USD, depreciating over 13 percent FY23TD.

With this, PKR has hit a record low against the USD, closing at 239.9 in the trading session on Thursday. On a calendar year-to-date (CYTD) basis, the PKR has lost almost 26 percent of its value against the USD.

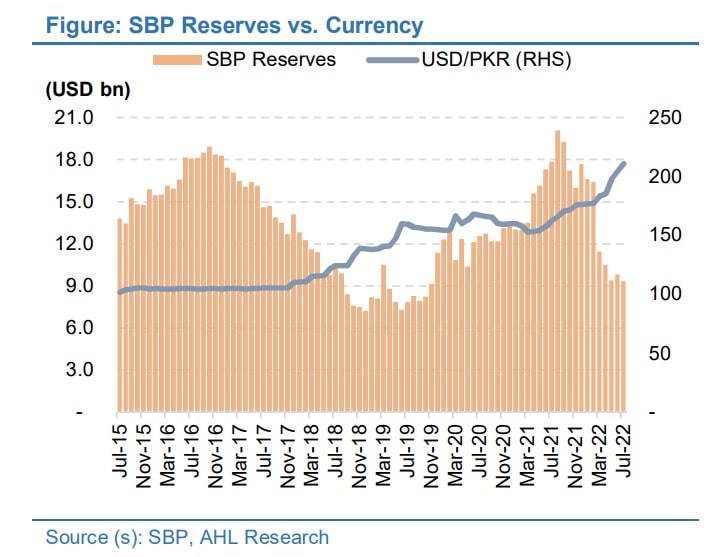

Another most important factor which has resulted in PKR depreciation is the widening of the current account deficit, which negatively impacts the country’s Balance of Payments position. This time (FY22), the current account deficit widened amid a surge in international commodities prices, along with strong domestic demand. Pakistan posted a $17.4 billion current account deficit in the outgoing fiscal year 2022 against $2.8 million in the same period last year.

However, this deficit is expected to come down to $11.1 billion in the current year with the measures taken by the fiscal and monetary authorities to slow down overall aggregate demand in the country.

REER and the Dollar index

According to the SBP, the PKR Real Effective Exchange Rate (REER) dropped to 93.57 in May 2022 from a level of 97 recorded in January 2022. With the recent depreciation, the report says that this level must have come down drastically, hovering in the 80s.

The movement in REER depends upon the nominal exchange rates of the basket currencies, their trade weights, and respective price indices. In addition to the PKR depreciation against the USD, a drop in REER is also explained by the 10 percent devaluation in major trading currencies (GBP and EUR) against the USD since Dec 2021.

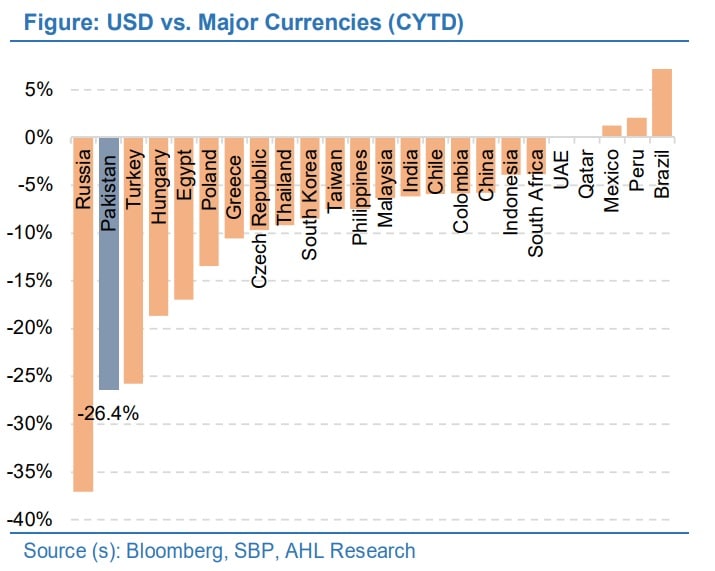

As mentioned by the SBP in its recent communique, the recent rupee depreciation against the USD is also in large part a global phenomenon. Globally, the USD has surged by 12 percent in the last six months to a 20-year high, as the US Fed has aggressively raised interest rates in response to rising inflation.

Future Outlook

The report says that the PKR still has inherent depreciation bias in the long term. However, in the short term, it expects some stability to be restored. The report attributes this short-term stability conditional upon inflows from bilateral and multilateral creditors, International Monetary fund (IMF) inflows, and strengthening of some macroeconomic variables including current account position along with State Bank of Pakistan’s (SBP) attempts to curb market speculation.

Is Pakistan Defaulting?

The report highlights that compared to what Sri Lanka did that led to a complete economic meltdown, SBP has time and again highlighted that the market concerns about the financial position and comparisons being drawn to the Sri Lankan situation have been ‘unwarranted’ and shall dissipate in upcoming weeks.

In a recent media interview, the acting governor stated that Pakistan’s external debt is low at around 70 percent of relatively long maturity and on comparatively easier terms with mostly concessional multilateral and official bilateral partners.

In addition, SBP has reassured that Pakistan’s $33.5 billion external financing needs for the current year (FY23) are fully met, with IMF in place.

Moreover, unlike Sri Lanka, Pakistan tightened its monetary policy and allowed the exchange rate to depreciate as soon as external pressures began. On the fiscal front, Sri Lanka’s fiscal deficits had been much worse than Pakistan’s, with primary deficits three to four times larger since the pandemic (12.2 percent of GDP compared to Pakistan’s 2.2 percent).

Moreover, the fear of default is not only limited to the forex market, in fact, the bond market yields too, in recent times, depicted panic and concerns of investors.

The yield of Pakistan’s international bonds has gone up significantly since April, especially the ones maturing in Dec 2022 and April 2024 trading at 45.8 percent and 44.1 percent respectively, (as of 29th July 2022).

The higher yields also point toward investors expectation of default despite Pakistan signing staff-level agreement for the combined seventh and eighth reviews of EFF with the IMF.

Moreover, the yields took a beating and came further under pressure with the downgrading of Pakistan’s outlook by the international credit agencies, Fitch and Moody’s, and S&P Global this week. All the agencies kept the rating unchanged, however, downgraded Pakistan’s outlook from stable to negative stating factors such as macroeconomic challenges and renewed political risks as key reasons.

The report says that as the maturity of the Dec 2022 bond is approaching, Pakistan in a normal scenario would have most likely issued a new bond to set off with the one maturing. However, with IMF in place, followed by inflows from other creditors, Pakistan might not consider reentering the international capital market in the current situation. To highlight, total bond maturities till 2024 are worth only $2 billion, with one maturing in Dec 2022 ($1 billion) and the other one in April 2024 ($1 billion).

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.

Yes

Knowledge