by Fahad Humayun

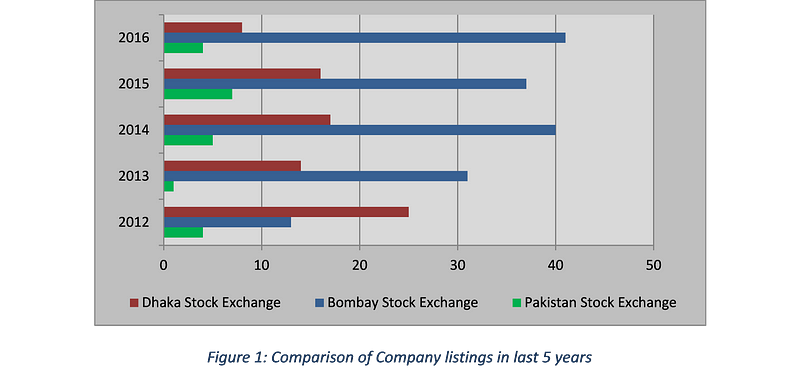

It’s been a decade since I started my banking career in Pakistan and the corporate scene hasn’t changed much. It’s still the same family groups, the same names, industries and limited depth. The stock exchange Index continues to be used as a barometer of economic progress and investor sentiment while new listings are rare events. In fact, to understand just how lacking the bourses are in terms of new listings, here is a comparison of new listings between Pakistan, Bangladesh and India.

Stock market listings are indicators of corporate growth, transparency, corporate governance and are permanent investments. Index growth on the back of Investor flows is a phenomenon driven by absence of proper taxation and audit controls as much as it is driven by economic growth and investor sentiment.

With a poorly functioning tax collection setup, a regressive tax policy that focuses on indirect taxation and more so no devolution of tax benefits down to the tax payer, there is little motivation to document businesses. As a result, small businesses focus on growth only through own sources so as to avoid disclosing the true strength of the business. The lack of professional talent working in the SME sector is also a cause of poorly managed books. SMEs are unable to attract talent due to the lack of organization structure, low payrolls and poor work culture.

Debt is a cheaper and quicker way of raising funds, but debt is not a growth driver

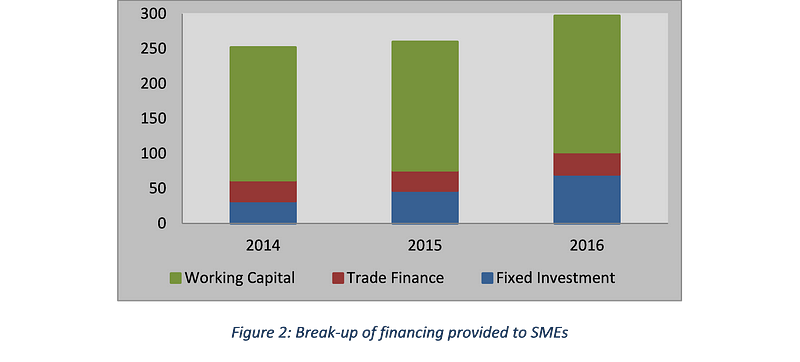

Business growth is derived from capital. Debt is a cheaper and quicker way of raising funds, but debt is not a growth driver as it eventually has to be repaid to be replaced by equity. Small businesses that hold the potential for rapid growth or even for steady growth face capital constraints. Due to the lack of professional management and record keeping, banks focus on short term working capital lending, instead of providing longer term funding for capital growth. The table below shows a breakup of the financing provided by banks in Pakistan to SMEs. Over 65% of debt financing is for working capital, and only in 2016 does the fixed investment financing crosses the 20% mark.

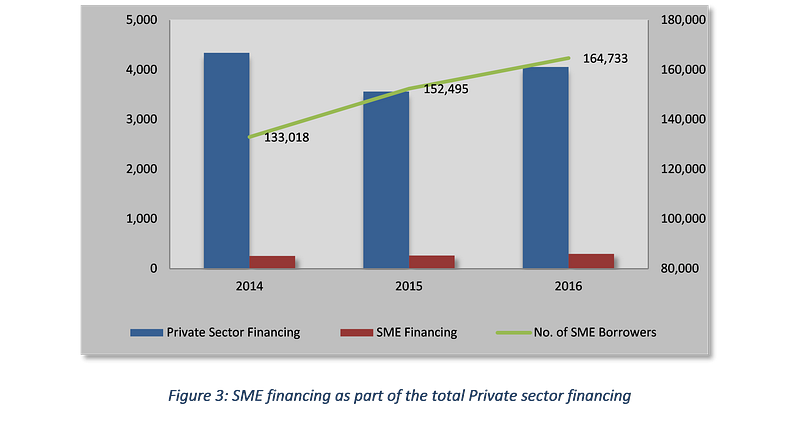

SME financing was a meager 7.3% of total Private sector financing in 2016

To better understand just how hesitant the banking industry is towards taking exposure to the SME segment, the table below shows that SME financing was a meager 7.3% of total Private sector financing in 2016. To put things into perspective, over 85% of all private enterprise falls under SME. Since 2014, banks have 31,714 new SME borrowers to their books which appear to be a decent number. However, it is interesting to note that number of borrowers between 2014 and 2016 has grown by 24% compared to SME financing which has grown by 18%, indicating reduced average exposures per SME client.

Creating Access to Capital for SMEs

Some of the key questions and hurdles that come to mind when we talk about getting Equity capital into a Small business are:

- Small Business owner is threatened that an outsider will take over control permanently

- Disclosures and audit will open a pandora’s box for the tax authorities that could result in lower profitability as well as legal issues

- Investor can’t trust the Small Business with the money and doesn’t have the resources to closely monitor it either

- Does the Small business have the human capital to manage the growth equity? Can it attract the right talent in the right time?

- With PSX offering such high returns, is investing in a growth SME really worth the time?

- What’s the legal platform protecting investment in private shares?

- What’s the EXIT? Is IPO the only route?

While the above is just a short list, a lot more questions are there for both the SME and the investor.

Finding a Solution

The roadblocks faced by SMEs are nothing new and all developing economies have had to tackle them. These boil down to 2 key elements, Capital and Human resources. Any country that has successfully found the solution to this conundrum has seen rapid growth for entrepreneurs and has gone on to create successful enterprises. The US is a leading example as it has a thriving Small business economy supported by Angel investors, Venture Capital, Private Equity, Hedge funds, Community banks and Investment Banks, each one playing a role to move companies up the growth ladder.

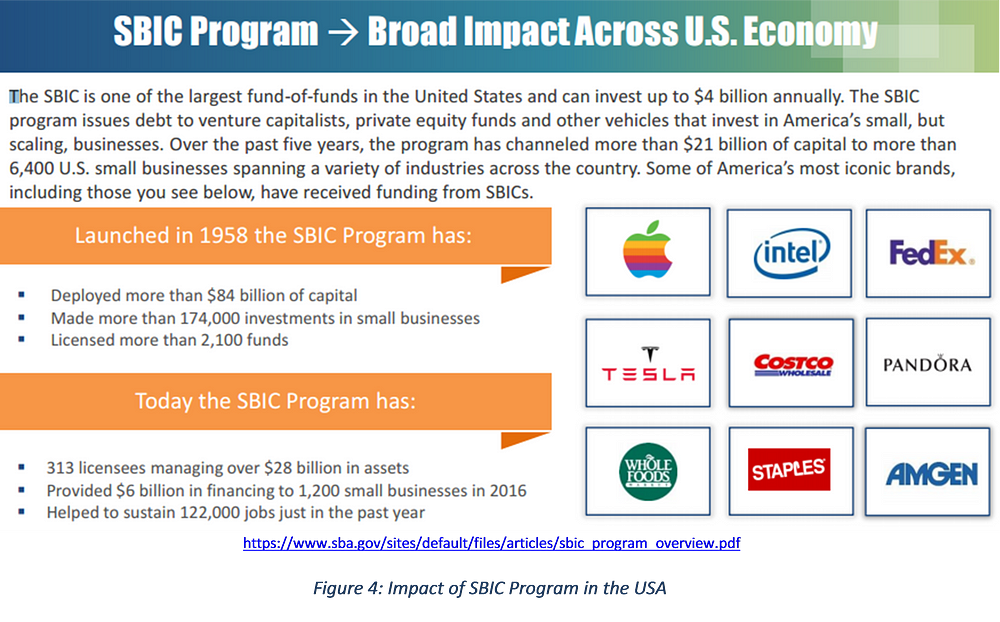

US Small Business Association (SBA) and the Small Business Investment Company (SBIC)

Realizing the need to channel money in to Small business, the SBA in 1958 launched the a SBIC Guarantee program. Under the program, Investment managers were offered a guarantee to raise debt from bank’s to invest as equity in to Small business. The guarantee was offered for an amount equivalent to investor money that the Investment manager would raise. So effectively for every $1 of investor money, $ 1 of Guaranteed debt was raised resulting in $2 investment in to the Small Business. The program started with a $1Bn Guarantee and has made a tremendous economic impact.

Replicating for Pakistan… With Some Tweaking

The benefit of the SBIC program in the US was that not only did it get money in to the Small businesses but the Investment managers got on as Board members and Senior Executives in these companies hence the problem of Human talent was also tackled. However, another key factor in the US was the availability of training and shared service resources that the SBA provided which allowed the businesses to focus on the core business instead of getting bogged down by the intricacies of legal and accounting overheads.

A similar program can be established in Pakistan with some tweaking so as to make it more adaptive to the local market.

1- The Guarantee:

Instead of waiting for a government body such as SBP to issue a guarantee program, the Corporate sector can be approached to pool in and create a single guarantee. The benefit for the Corporate guarantors will be:

· The Guarantee itself can be a Non-funded CSR activity

· Each Guarantor will be given the opportunity to identify SMEs that form its own value chain for equity funding. This means that a Corporate can identify which companies it needs to grow to sustain its own growth. For instance, if a Corporate is expanding its own production line, then instead of adding more vendors on the supply chain, it could support the growth of an existing well performing vendor.

· A training ground for own management and for the value chain. Each Guarantor will also have to commit certain number of man-hours that its employees will pitch in to train and guide the companies that are funded by the program. Hence, it’s a great way for a Corporate to interact with its own value chain and it helps its own employees to learn training and mentoring skills

· To maintain transparency, the guarantee will have to be Blind Pool and all guarantors will have equal rights at all times. The decision to fund or not to fund a certain company will not be with the guarantors. This decision will at all times remain with the asset manager and the guarantors will have to accept the investment decision as long as it is in line with the set guidelines.

2- The Investment Company:

In my initial meetings with some of the existing Asset Management Companies, they have shown great interest in the idea and already they are exploring ideas on how to enter in to the VC market. The growth of AMCs has been slow at best as they are stuck with limited asset classes and have been re-packaging and re-branding the same over and over again. With Debt, Govt bonds and deposit rates at an all-time low, the time is right to find alternate asset classes that can provide strong earnings.

The Guarantee program would work by screening the AMC interested in working under the program. The AMC would setup a fund as per regulations and an SPV to hold the private shares. Fund life would be a maximum of 10 years with an objective to exit each investment within 5 years of entry.

3- The Lender:

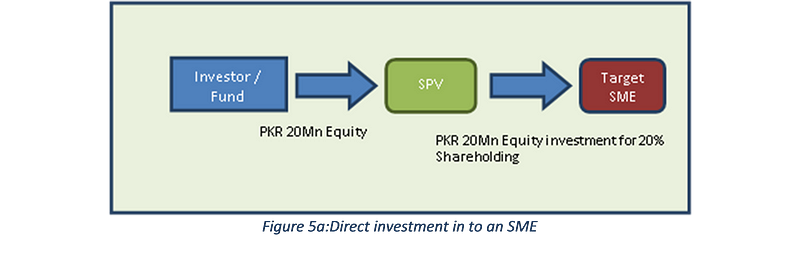

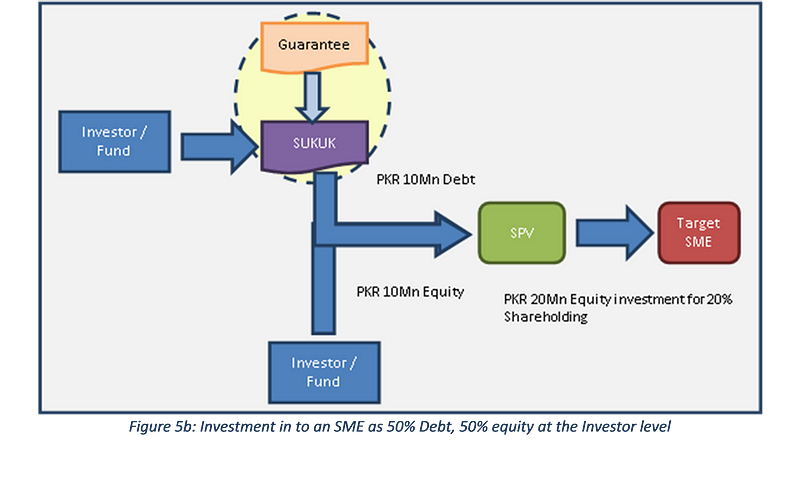

The lenders can be banks, DFIs or any entity authorized to lend under the regulations in the country. Another twist on this matter can be the creation of SUKUK bonds for the debt. By doing so, the door is open for any entity to be the lender. One approach can be that Investor himself is also the lender. Refer to below illustrations:

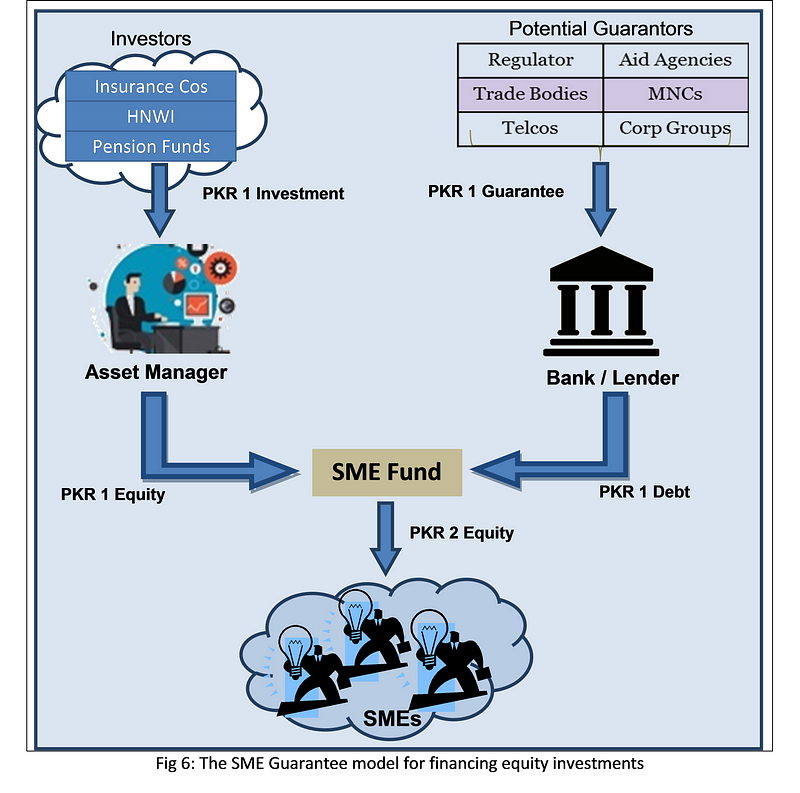

Putting it All Together

Based on the points discussed above, below is the conceptual layout of how the program would function.

Key Features:

- Government and/or Corporate based Guarantee program that will secure debt to SME Funds (VC & Private Equity)

- 1:1 Leverage against Investor commitment

- SPV structure to acquire private shares of target SMEs

- Fund tenor and Debt tenor will be 7 to 10 years

- Funds to invest in identified SME sectors and monitored against KPIs

For a more detailed view of the program and its benefits check out the below presentation

The author has recently concluded work on financing the first Sharia’h compliant Leveraged SME Investment fund for SAR 450Mn under a Guarantee program replicating the US-SBIC model in Saudi Arabia. He can be reached here