About 100 million adults in Pakistan don’t have access to formal and regulated financial services. This number accounts for about 5% of the world’s unbanked population, which stands at 2 billion, says the World Bank (WB).

Having a formal and regulated transaction account opens access to other financial services, such as savings, payments, insurance and credit, all of which can help people better manage their lives and reduce poverty.

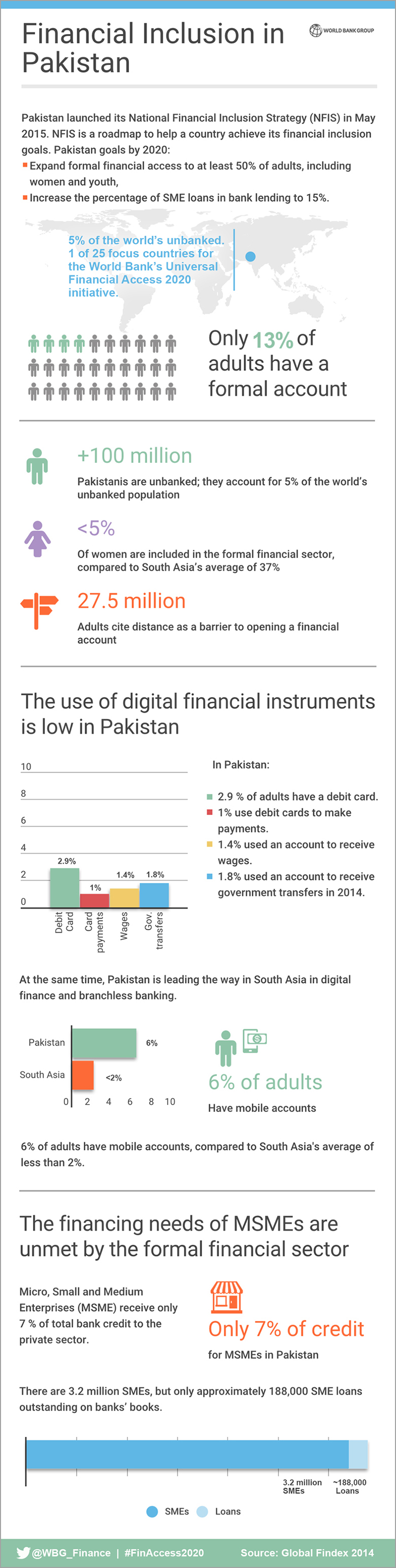

In May 2015, Pakistan launched its National Financial Inclusion Strategy (NFIS), a roadmap to help a country achieve its financial inclusion goals.

Pakistan’s goal is to achieve universal financial access, with a headline NFIS target of expanding formal financial access to at least 50% of adults, including women and youth, and to increase the percentage of SME loans in bank lending to 15% by 2020.

Pakistan’s financial inclusion strategy is currently focusing on four areas:

- Promoting digital transaction accounts and reaching scale through bulk payments

- Expanding and diversifying access points

- Improving capacity of financial service providers

- Increasing levels of financial awareness and capability

World Bank Group said that it is supporting these country-led efforts, which are reflected in Pakistan’s Country Partnership Strategy (2015-19), with reforms and other actions to expand financial access and inclusion.

Pakistan is also among the 25 countries the World Bank Group and partners are prioritizing as part of the efforts to reach Universal Financial Access by 2020.

Pakistan’s Financial Access Statistics

- Only 13% of Pakistani adults have a formal account, according to Global Findex 2014.

- Less than 5% of women are included in the formal financial sector, compared to South Asia’s average of 37%.

- More than 100 million Pakistanis are unbanked; they account for 5% of the world’s unbanked population.

- 27.5 million of Pakistani adults cite distance to a financial institution as a barrier to opening a financial account.

- The use of digital financial instruments is low.

- 2.9 % of adults in Pakistan have a debit card, and only 1% of adults use them to make payments.

- Only 1.4% of adults use an account to receive wages and 1.8% of adults use it to receive government transfers in 2014.

At the same time, Pakistan is leading the way in South Asia in digital finance and branchless banking.

- 6% of adults have mobile accounts, compared to South Asia’s average of less than 2.6%.

The financing needs of MSMEs are unmet by the formal financial sector.

- Micro, Small and Medium Enterprises (MSME) receive only 7 % of total bank credit to the private sector.

- There are 3.2 million SMEs, but only approximately 188,000 SME loans outstanding on banks’ books.

Selected Measures to Improve Financial Access in Pakistan

World Bank Group has proposed Pakistan following action items to enhance financial access in the country:

- Shift all government-to-person payments from cash to digital payments, following the success of the Benazir Income Support Program in opening up access to financial services.

- Create incentives for the private sector to use electronic payments instead of cash when paying for private sector invoices and salaries.

- Build on the success of Easypaisa. Twenty million customers conduct nearly 650,000 through Easypaisa, which is accepted over 75,000 shops in more than 800 cities across the country.

- Establish a consistent regulatory and oversight framework for all payment and settlement systems, for banks and non-banks.

- Develop legal frameworks for secured transactions, factoring and credit reporting systems, and an electronic movable collateral registry.

- Establish an enabling regulatory and supervisory framework for the non-bank financial sector, including Islamic financial service providers, supported by adequate financial consumer protection.

- Expand access points to banks through agent networks or partnerships with microfinance institutions or postal networks.

- Improve financial education and literacy outreach, particularly among people who have little experience with the formal financial sector and digital payments

Recent World Bank Group’s engagement on financial inclusion

The Bank Group’s past support to the country has enabled it to strengthen its banking system and increase private sector participation. IFC investments have supported nearly 9 million customers through the private sector in expanding access to financial services to women and to micro, small, and medium enterprises. Some of the recent engagements include:

- Supporting the development of the National Financial Inclusion Strategy in 2015, supplementing it with nine technical notes on agriculture finance, MSME finance, digital transactional accounts, housing finance, Islamic finance, payments systems, secured transactions, insurance and pensions.

- Ongoing policy reforms through a Development Policy Credit series to support legislative actions (credit infrastructure, secured transactions, foreclosure) and state-owned insurance sector reforms.

- Financial Inclusion Support Framework to support implementation of the NFIS and expand access to financial services. In December 2015, Pakistan approved theCountry Support Program (CSP) to help achieve financial inclusion goals stated in its NFIS.

- Pakistan Poverty Alleviation Fund (PPAF) Investment Lending Project created the apex institution to develop and provide financing to the microfinance sector. TheWord Bank has supported PPAF since 2000. Since its inception 10 million vulnerable and marginalized people have benefitted from the program interventions, with over half of them being women.

- Pakistan: Social Safety Net Project: Almost 4.8 million poorest households receive US$15 in monthly cash transfers through the Benazir Income Support Program (BISP), Pakistan’s flagship national safety net system. By the beginning of 2015, more than US$2.9 billion was disbursed to BISP beneficiaries where 93% of them received the cash transfers through technology-based payments, such as debit cards and mobile phones.

- WomenX is a pilot program supporting women entrepreneurs in Pakistan by providing business education and support services to women running small and medium-sized enterprises in Karachi, Lahore and Peshawar.

Stay Connected with ProPakistani

Get the latest news, tech updates, telecom insights, and business stories wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.

kon si dunya se aay ho bhai, jahan peenay ka saf pani nahi, hospital mein beemar k liyay bed nahi aur ghareeb k bachay k liyay education nahi, wahan financial services na b ho to chalta hy!

Adult ka kuch alternative word use kr lete, bar bar Adult word parh k lag rha hey jese kisi Adult film ki bat horhi hey