Oil and gas sector earnings are projected to increase during 1QFY23 primarily because of higher oil prices, elevated dollar indexation, and exchange gains due to the strengthening of the dollar on a sequential basis.

According to Foundation Securities, the sector’s profits are expected to grow by 46 percent YoY in 1QFY23, with the Oil & Gas Development Company (OGDC) set to outperform peers with earnings growth of 50 percent YoY in 1QFY23.

Impact

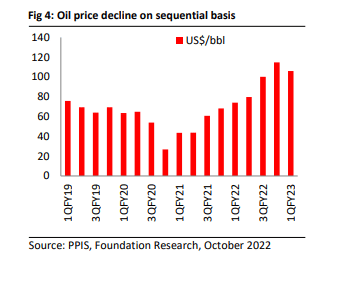

According to the report, higher oil and dollar indexation will propel earnings growth. Oil prices declined on a sequential basis in 1QFY23 from its peak quarterly average of US$ 114.82 in 4QFY22 on the back of higher inflation and higher interest rates in the West combined with lockdowns in China. However, oil prices are still higher by 43 percent YoY to average at US$ 106/bbl in 1QFY23 due to fear of lost Russian barrels.

There’s a production decline across the board due to supply chain disruption on the back of the unprecedented monsoon season. The report said oil production in the space is already down by 10 percent YoY primarily because of a decline in production from Adhi (~23 percent YoY), TAL (~4 percent YoY), Nashpa Field (~2 percent YoY), and KPD field (~6 percent YoY).

FSL E&P universe gas flows declined by a mere 0.2 percent YoY given lower flows from KPD (~1.0 percent YoY), TAL (~11 percent YoY), Uch (~15 percent YoY), MARI (~3 percent YoY), and Sui (~8 percent YoY). However, gas flows from Qadirpur and Kandhkot fields increased by ~5 percent YoY and 2.2x YoY in 1QFY23.

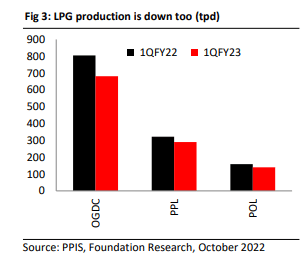

In line with oil production, LPG production is down by 14 percent YoY in 1QFY23 primarily because of lower production from TAL Block (~11 percent YoY), Adhi (18 percent YoY), and KPD (~39 percent YoY).

Listed Companies Offer Support

OGDC is widely expected to lead the earnings growth. The company may post earnings per share (EPS) of Rs. 11.7, up 50/132 percent YoY/QoQ, in 1QFY23 mainly due to higher dollar indexation and exchange gains despite production decline across the board. The report expects OGDC to announce a dividend of Rs. 2 per share

More research suggests that Kandkhot flows will support growth in the sector. Pakistan Petroleum Limited (PPL) is likely to post an EPS of Rs. 8.9, up by 1.4x/18.8x YoY/QoQ, in 1QFY23 given higher gas flows on rejuvenation of flows from the Kandhkot field and higher dollar indexation. The company’s gas production increased by 12 percent YoY as flows from Kandkot field improved by 2.2x YoY.

Mari Petroleum Company Limited (MPCL) will likely post improved profitability for the quarter. MPCL is projected to post an EPS of Rs. 96.9, up 42 percent/2.3x YoY/QoQ, given higher gas prices for MARI HRL base and incremental flows amid elevated dollar indexation. However, flows from the field are expected to be down 3.2 percent YoY due to lower offtake from fertilizer plants on the back of maintenance.

Oil prices have a significant role to play in driving earnings growth in the sector. According to the report, the profitability of POL products in 1QFY23 is expected to clock in at Rs. 27.3, up by 48 percent YoY, given elevated oil prices and higher dollar indexation. POL production is down across the board mainly because of TAL Block.

Outlook

The sector is widely touted to outperform various other publicly traded companies on the benchmark KSE-100 index given elevated oil prices amid the rationalization of gas prices. Lower operating costs, debt-free balance sheet, dollar-hedged revenue, and improved security situation further support the outlook.

Stay Connected with ProPakistani

Get the latest business news, market insights, and economic updates wherever you prefer.

Add ProPakistani to Preferred Sources and see more of our stories in Google Search and Top Stories.